3

3

Welcome to our institutional newsletter, Crypto Long & Short. This week:

- Alec Beckman on why $BTC-backed lending is not a crypto story, but a capital efficiency story.

- Serena Sebastiani on how stablecoins aren’t a crypto product; they’re becoming the settlement infrastructure global finance forgot.

- Top headlines institutions should pay attention to by Francisco Rodrigues.

- “Ethena's Solana lending markets cross $1B in 4 days” in Chart of the Week.

Thanks for joining us!

-Alexandra Levis

Expert Insights

Bitcoin-backed loans belong in the cost-of-capital conversation

By Alec Beckman, VP of the Americas, Psalion

The argument is not about whether to buy bitcoin or not. It is for advisors, real estate investors, small business owners and founders who already own it, or work with clients who do. The practical question is simple: if a client carries meaningful debt, why is $BTC-backed lending not in the capital stack discussion? Debt-heavy professionals already compare collateral, rate, fees, speed and covenants. Bitcoin-backed loans should be evaluated the same way.

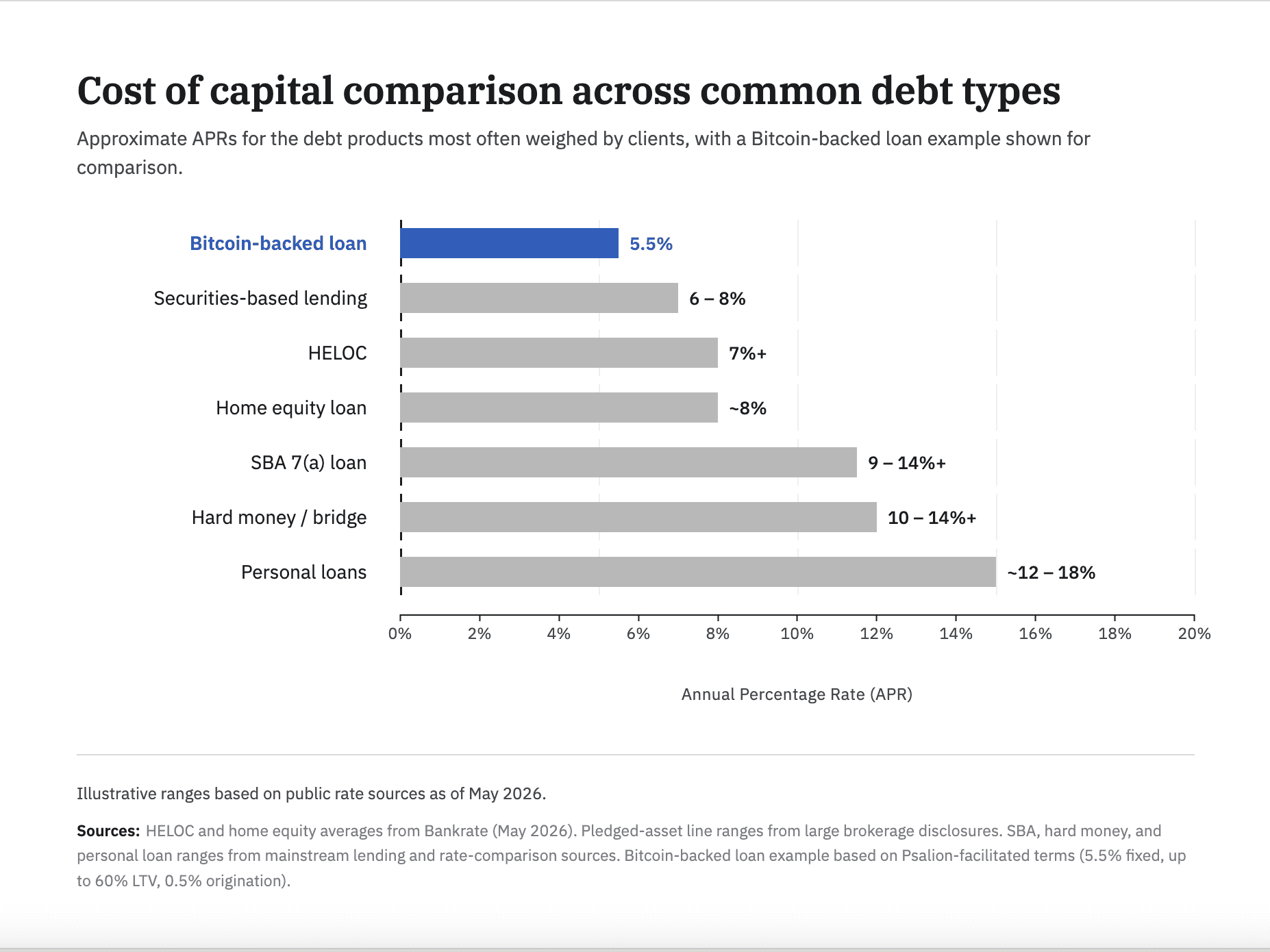

The debt menu is familiar. HELOCs are tied to home equity, often variable, and currently sit above 7% for many borrowers. Hard money and bridge loans can move quickly, but often price around 10% to 14% plus points. Securities-based lending can be efficient, but rates often begin around 6% to 8% and require sizable brokerage assets in one place. Personal loans frequently land in the low-to-mid teens. SBA loans can be useful, but the all-in cost, documentation and time to fund are not trivial.

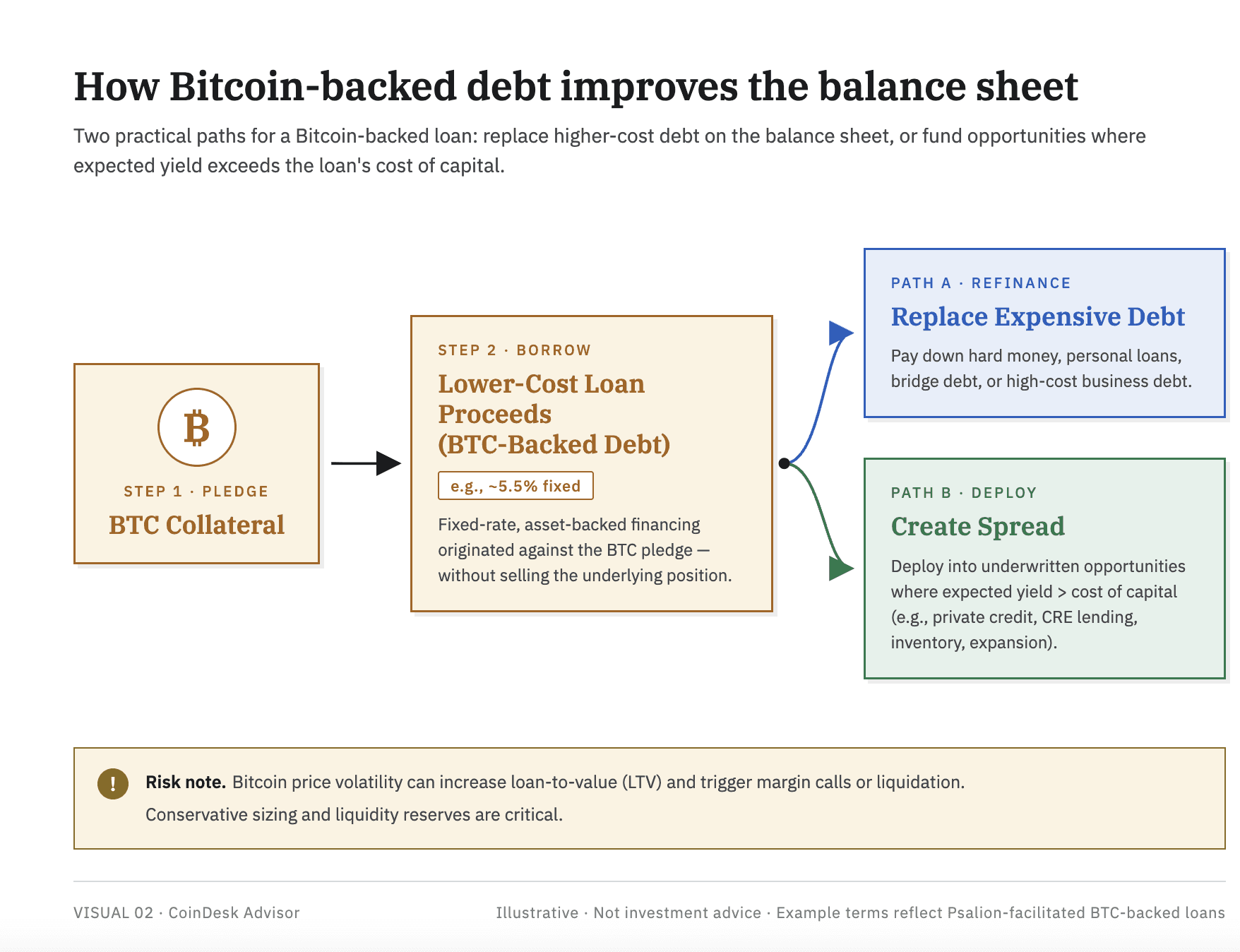

Bitcoin-backed lending changes the collateral, not the math. The borrower pledges $BTC, receives dollars or stablecoins and repays under agreed terms. The asset is liquid, verifiable and easy to monitor. Market rates still vary widely, but more competitive structures are emerging. At Psalion, for example, we facilitate access to Bitcoin-backed loans at a 5.5% fixed rate, up to 60% LTV, with a 0.5% origination fee. That is one data point, but it shows why the category belongs in a serious debt comparison.

Rate matters first. For someone already holding $BTC, the relevant question is not “Should I borrow?” It is “Where should I borrow?” Against a house? A business? A securities portfolio? Or $BTC? If $BTC collateral produces cheaper capital than the borrower’s existing debt, it can reduce the blended cost of capital.

Fees matter next. Hard money can carry points on origination. SBA structures can include guarantee fees, closing costs and advisory costs. Personal loans may embed higher APR through origination. Lower fee bitcoin-backed lending can make the all-in economics materially cleaner.

Friction matters too. Traditional credit often requires income verification, tax returns, appraisals, operating statements, personal guarantees, covenants and time. $BTC-backed lending is collateral-first. The collateral can be verified quickly and monitored continuously. Faster access to liquidity is not just convenience. It can change the economics of a refinance, acquisition, tax payment or bridge need.

Advisors should care because $BTC is now part of more client balance sheets. Too often, $BTC sits idle while the same client pays higher rates elsewhere. If the client can borrow against $BTC and replace more expensive debt, the advisor has improved the balance sheet without forcing a sale and potentially creating a taxable gain.

There is a second use case: yield on spread. Some real estate investors, founders and business owners see opportunities where expected returns exceed their cost of capital, such as private credit, commercial real estate lending, inventory or operating expansion.

Borrowing against $BTC to pursue those opportunities can make sense when the borrower understands both sides of the trade: the yield opportunity and the collateral risk.

That risk is real. Bitcoin is volatile. If the price falls enough, LTV can breach agreed thresholds and trigger margin calls or liquidation. Liquidation can create a taxable event. This is not for every client. It is for borrowers who understand $BTC volatility, maintain liquidity and size loans conservatively below maximum LTV.

For clients who already own bitcoin and already carry debt, $BTC-backed lending is not a crypto story. It is a capital efficiency story. Ignoring it may mean leaving cheaper capital, or a valuable spread opportunity, on the table.

Principled Perspectives

Stablecoins are now infrastructures

By Serena Sebastiani, chief strategy officer and head of government and regulatory affairs, Fuze

There's a kind of financial friction that becomes invisible when you live inside it long enough.

From New York or London, cross-border payments work. From Nairobi, Jakarta or Almaty, they don’t.

An SME in Nairobi pays a supplier in Karachi. The money leaves Monday. It arrives Thursday. Along the way it passes through two correspondent banks, absorbs fees on both ends, gets hit with an FX spread on the USD conversion and triggers multiple compliance checks. Both the buyer and the supplier absorb the friction by pricing it into the deal and extending the credit note.

This is how it actually works to operate across the fastest-growing trade corridors globally: Gulf to South Asia, intra-African trade, CIS to MENA, and Southeast Asia remittances.

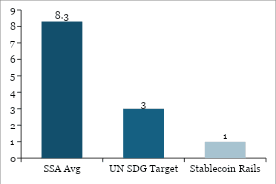

Multiply that by the $136 billion SME trade finance gap in Africa alone. Multiply it by the $100 billion in annual remittances flowing into the continent. Multiply it across the Gulf-to-South-Asia corridor, CIS-to-MENA and intra-ASEAN. And also account for the cost of sending money into Sub-Saharan Africa, which remains the most expensive region in the world, at 8.3% on average (almost three times the UN’s 3% target). In live corridors today, stablecoin rails are already operating at under 1%. What we're looking at is not simply a matter of optimizing the margins, but a structural gap in the fastest-growing regions of the global economy.

SWIFT was built for a specific world: large banks, large tickets and major financial centres. It works perfectly for that world. Yet the supplier payment in Nairobi, the remittance from Riyadh to Manila, or the trade settlement between Almaty and Istanbul has been making do with infrastructure designed for someone else's economy.

That's the gap stablecoins are moving into, and they’re not a product but real plumbing.

Chart 1: The Remittance Cost Gap

Sources: World Bank (Q1 2025); UN SDG 10.c; Transak / Operational corridor data

What we observe from the ground

I spent time with regulators and market operators across high-growth corridors and a pattern that emerges is that people closest to the friction are the least ideological about the solution. They are the ones actually trying to integrate stablecoins into the existing financial system.

In Kigali for example, the framing isn't “crypto adoption.” Rwanda's National Bank launched a CBDC pilot in February with cross-border interoperability as the explicit design priority. A draft Virtual Assets Law now in parliament applies a clean two-tier structure: Central Bank oversight for payment stablecoins and Capital Markets Authority for investment instruments. A fintech license passporting agreement with Kenya, signed in March, is already being designed as a template for the East African Community. This is regulatory infrastructure being built with precision, for a specific problem, by people who understand their own market.

The insight is not Rwanda-specific, but Africa-wide, where mobile money already functions as the default financial layer. With over a billion registered accounts, 96% financial inclusion in markets like Rwanda, this distribution infrastructure took decades to build. What mobile money never solved for is cross-border interoperability. Stablecoins fit that gap naturally, not replacing fiat currencies, but acting as the settlement layer that makes mobile money efficient.

The same logic, four corridors

Middle East

The Central Bank of UAE’s Payment Token Services Regulation treats stablecoins as settlement infrastructure rather than speculative securities. That regulatory framing is practical and allows banks to issue AED stablecoins that can be used directly as a means of payment, and banks and licensed fintechs can build on stablecoin rails without treating every transaction as a liability. In this way, the Gulf stablecoin settlement is happening inside regulated perimeters.

CIS markets

In Kazakhstan, Uzbekistan and Georgia, the driver is dollar access. Domestic currency volatility creates structural demand for USD, and formal banking doesn't reliably provide them. Stablecoin adoption here is dollarization leveraging a new distribution channel. The institutional opportunity is providing that access inside a compliance framework, with the custody and reserve standards that make it durable.

Southeast Asia

In Southeast Asia, the driver is cost and speed. In corridors like Gulf-Indonesia or Gulf-Philippines for remittances, stablecoin rails eliminate the need for pre-funding and speed up settlement from days to minutes (often under 20 minutes, 24/7). Cost reductions of 40–80% are already observable in operational flows.

I engaged with regulators, banks and fintechs in these markets. The question here is: how can we facilitate higher volumes on stablecoin rails and give back to the households?

Africa

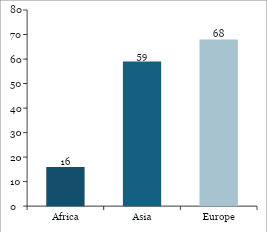

Remittances are expensive, but the B2B case is urgent as well. Intra-African trade only accounts for 16% of total trade, against 68% for Europe and 59% for Asia. The AfCFTA created the legal architecture for a $3.4 trillion market, but the payment infrastructure hasn't kept up. Chinese traders sourcing African goods are already settling in USDT because it is superior for their transaction sizes and timelines. To make this properly institutional and largely adopted, the essence is to guarantee that the activity happens compliantly, with proper rails.

Chart 2: Intra-Regional Trade Share — Africa vs Peers

Sources: UNCTAD / AfDB / WTO; World Bank / African Union (AfCFTA projection)

Stablecoins are infrastructure

Global banks and fintechs are still largely approaching stablecoins as a product to distribute to customers. The more significant opportunity is treating them as infrastructure to build on, particularly in remittances and B2B payment flows: treasury management, supplier payments and FX settlement. These are flows where the speed improvement and cost reduction are measurable (minutes vs days, basis points), and where the compliance trails on well-designed digital rails are demonstrable and trackable. These include on-chain transaction monitoring, wallet attribution and automated regulatory reporting that produces a compliance record that informal transfer channels structurally cannot. The data generated by these rails is what gets correspondent banking relationships restored in markets where de-risking has cut them.

Solving the friction

What remains to be solved for the infrastructure to properly work at scale? Regulatory frameworks that define reserve standards and redemption rights, cross-border supervisory coordination and AML/CFT laws interoperability.

All this is being worked through, and more in the market that matters (high-growth) than in established developed countries.

From experience working with regulators and now proactively engaging with them, I learned that the pattern that works is: 1. A phased licensing framework that lets regulators learn alongside the market; 2. Proportionate requirements scaled to institutional size and risk profile; 3. Bilateral passporting agreements that make compliance portable across corridors.

The corridors where this infrastructure is most needed are not waiting for global standards to arrive but are actively building. The question for global institutions is whether they're part of that architecture or arriving late to fintech-leading infrastructure.

Headlines of the Week

Francisco Rodrigues

This week's headlines show structural progress on Wall Street's onchain push, with a market-structure bill clearing its biggest hurdle, JPMorgan extending its tokenization stack, and asset managers tackling the redemption-speed problem. Solana has meanwhile kept quietly cementing its infrastructure for institutional use.

- Clarity Act clears U.S. Senate committee, on its way to a final test in Congress: Chairman Tim Scott secured a 15-9 bipartisan vote with Democrats Gallego and Alsobrooks crossing over, though unresolved law enforcement and government-ethics provisions still stand between the bill and a floor vote before the summer recess.

- JPMorgan files to launch new tokenized fund as Wall Street tokenization race heats up: The Ethereum-based JLTXX fund, run through JPMorgan's Kinexys blockchain unit, is structured to satisfy GENIUS Act stablecoin reserve requirements — landing days after BlackRock filed for its own tokenized Treasury vehicle.

- BlackRock, Janus Henderson tokenized funds get instant redemptions with new $1 billion facility: Grove's Basin facility advances stablecoin liquidity against approved redemptions from BlackRock's $2.2 billion BUIDL and Janus Henderson's $1.1 billion JTRSY, targeting the multi-day settlement gap that has held back the $15 billion tokenized Treasury market.

- Mike Novogratz's Galaxy receives New York BitLicense for institutional crypto push: NYDFS cleared GalaxyOne Prime NY to serve hedge funds, RIAs and family offices on a $9 billion platform, making Galaxy only the second firm to win a BitLicense in 2026 after Strike.

- Solana is shedding its memecoin reputation as big banks move billions into its ecosystem: A Messari report shows Solana's tokenized RWA market cap jumped 43% QoQ to $2.01 billion, with BlackRock's BUIDL, Ondo, Franklin Templeton and a Citigroup-PwC trade finance PoC live on the network, alongside payments integrations from Visa, Stripe, PayPal and Western Union.

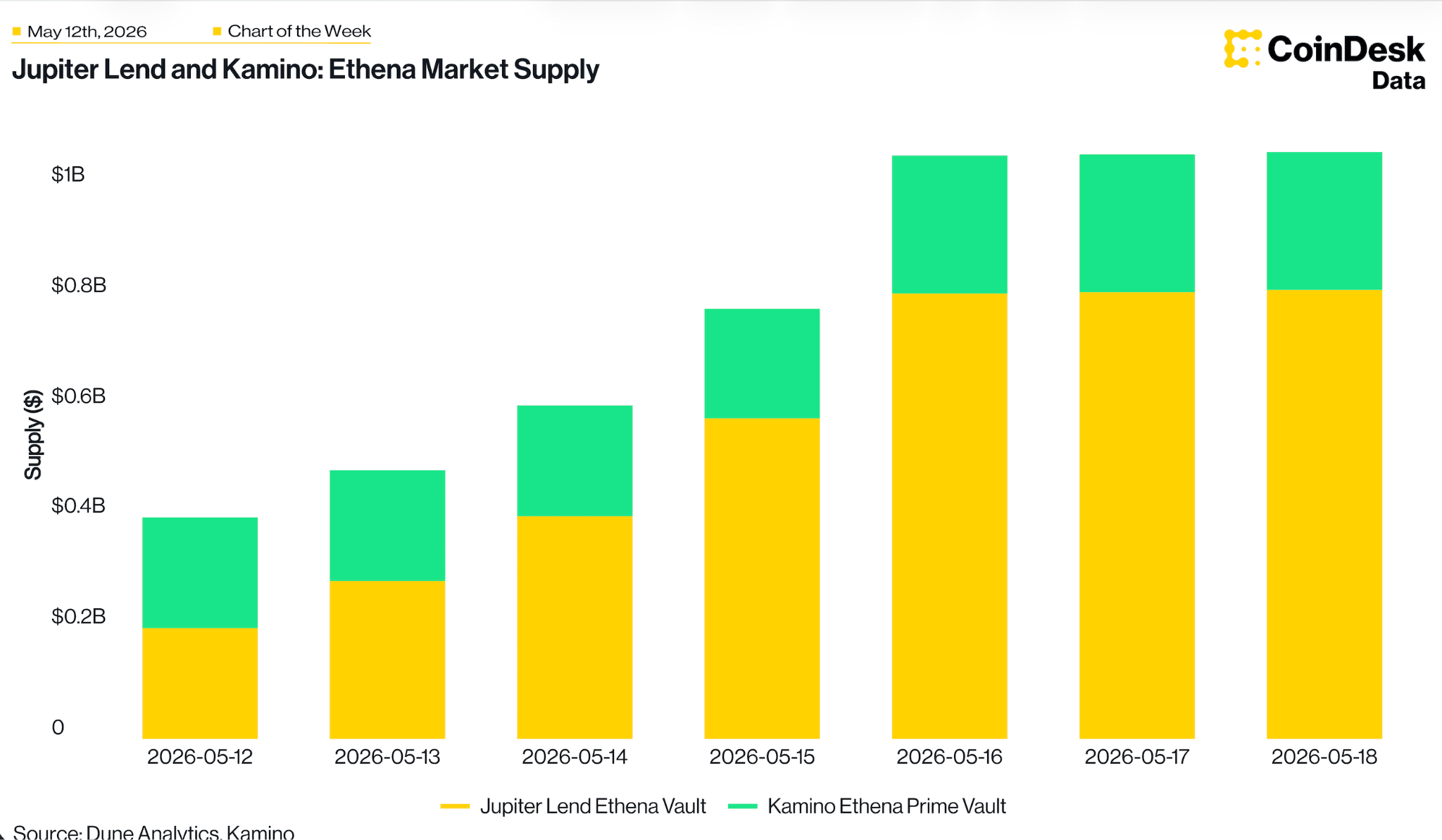

Chart of the Week

Ethena's Solana lending markets cross $1B in 4 days

Combined USDe and USDG supply across the Bitwise-curated Jupiter Lend market and the Kamino Ethena market rose from $401M on launch day (May 12) to $1.06B on May 16 - driven almost entirely by looper-led growth on Jupiter Lend, where supply climbed from $201M to $812M while Kamino's Ethena Prime vault held steady around $250M.

Listen. Read. Watch. Engage.

- Listen: Did you hear? CoinDesk's May 2026 Exchange Benchmark report from CoinDesk Research was released last week. The standards have been raised and our research team breaks down the ratings.

- Read: In Crypto for Advisors, Sam Boboev, Founder & CEO at Fintech Wrap Up explains how stablecoins are becoming the payment rails in the digital economy.

- Watch: Videos are live from Consensus 2026 by CoinDesk. Rewatch a favorite global thought leader onstage or watch for the first time!

- Engage: CoinDesk will be at the Women in Digital Assets Forum (WIDAF) in NYC on June 3. Let’s connect onsite!

Looking for more? Receive the latest crypto news from coindesk.com and market updates from coindesk.com/institutions.