14

14

Wall Street’s crypto footprint has never been larger. BlackRock alone reported nearly $150 billion in digital asset-linked AUM in its 2026 chairman’s letter. Public companies hold over 1.1 million $BTC on their balance sheets. Institutions disclose more than 513,000 $BTC through ETF wrappers.

Yet aggregate numbers obscure the question that matters most. Who actually holds what, through which infrastructure, and why?

This article maps Wall Street’s crypto ownership across five layers.

It starts with SEC 13F filings, moves through corporate balance sheets, follows the money into tokenized fund rails, traces the custodial chokepoints where keys concentrate, and ends where filings go dark, with on-chain OTC flows that reveal holders no quarterly report captures.

SEC 13F Filings Reveal Secrets About Wall Street Crypto ETF Holdings

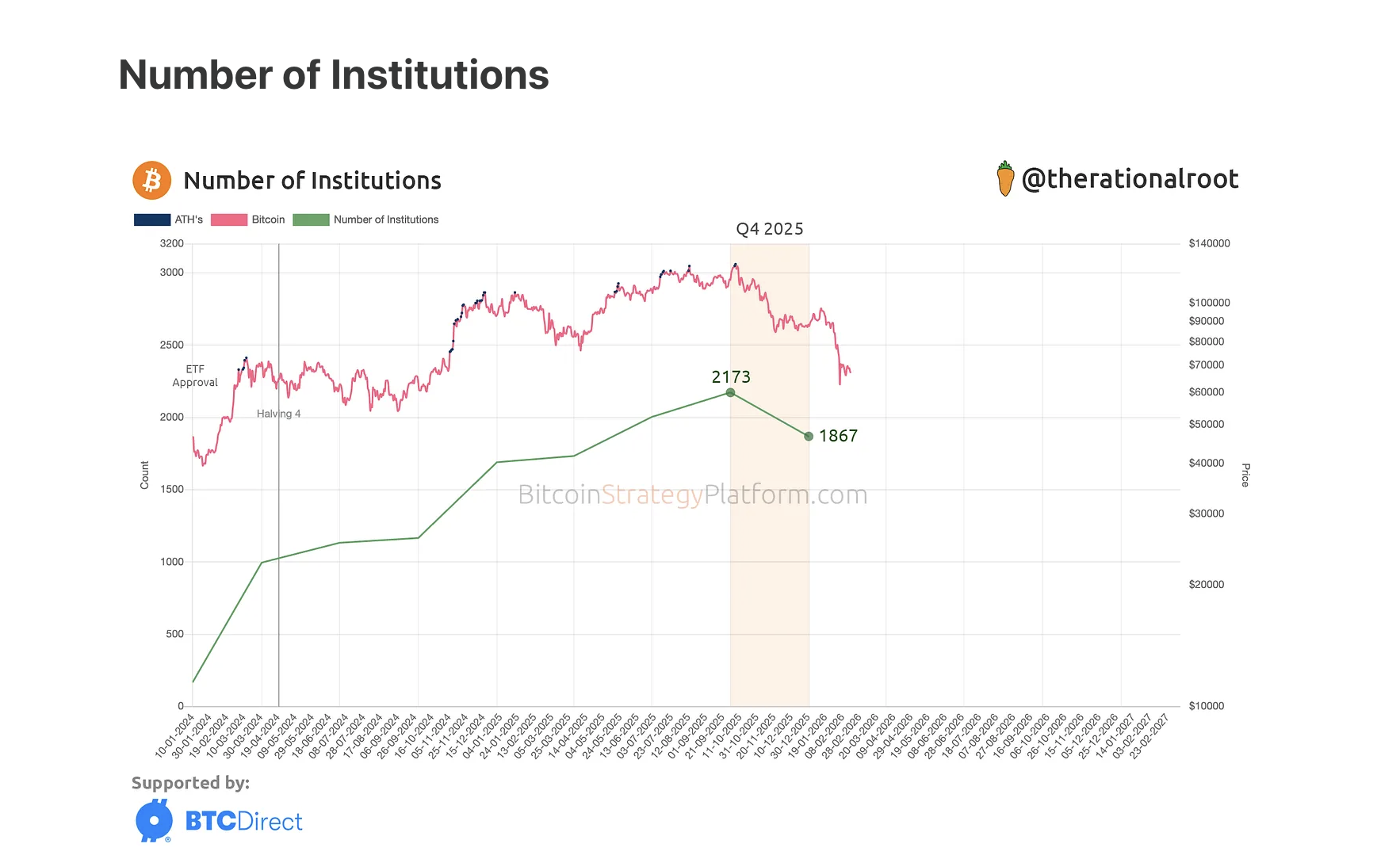

Despite a 23% price decline in Q4 2025, global Bitcoin ETF flows remained positive at $3.7 billion. Full-year professional ETF ownership grew 32% versus 18% for the broader ETF investor base.

Institutions still held over 513,000 $BTC through ETFs, though filer count declined from 2,173 to 1,867.

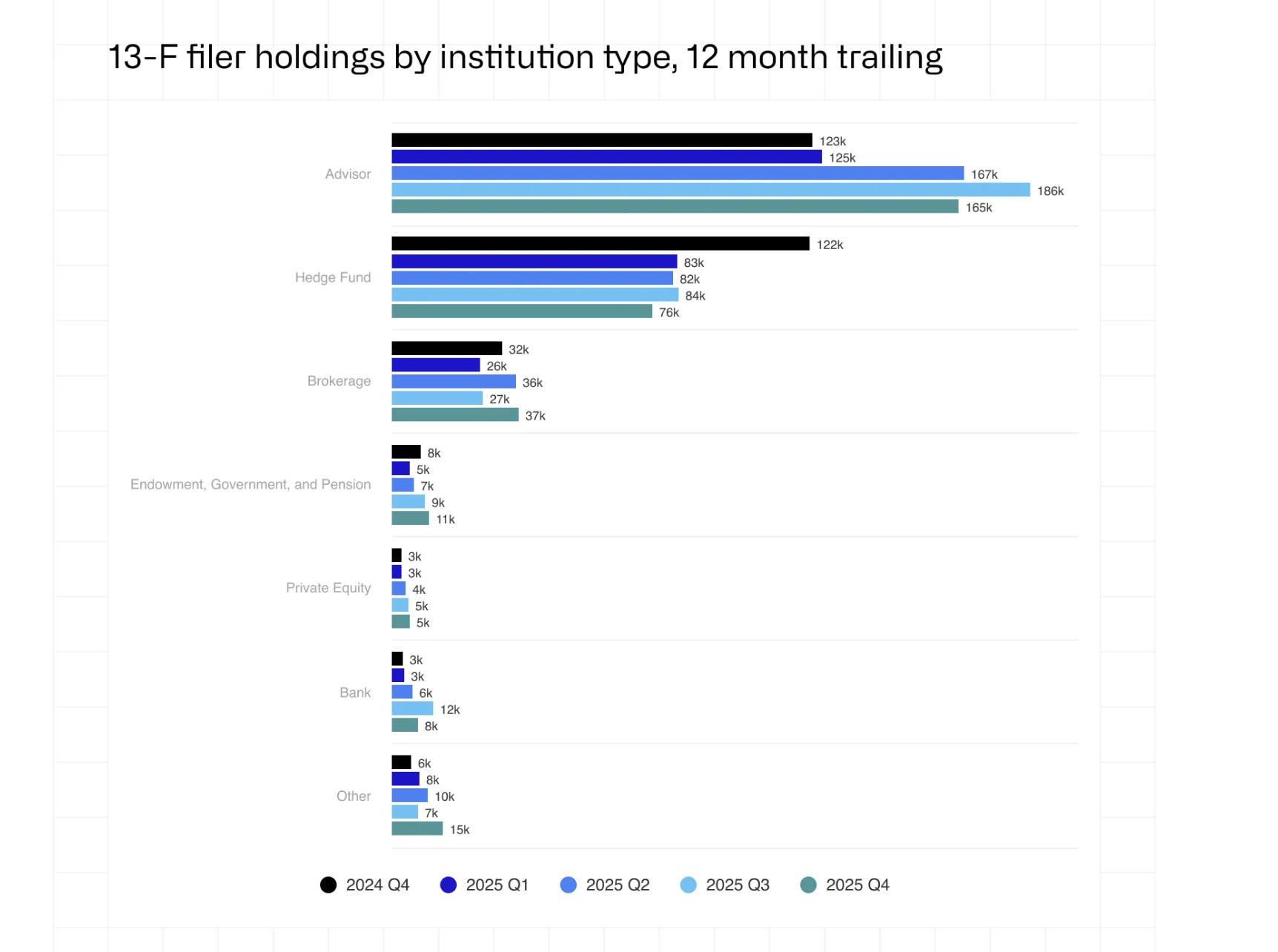

Not all of this is conviction capital. The basis trade, a strategy involving a long spot ETF position paired with a short CME futures position, has been a primary institutional strategy since ETF approval.

Hedge fund exposure declined nearly 10% in Q4, as leverage unwound and the basis spread narrowed.

Cohort rotation, not capitulation, defined Q4. Millennium added 8,100 $BTC. Abu Dhabi’s Mubadala added 2,300 $BTC. Morgan Stanley added 1,900 $BTC. Dartmouth became the fourth Ivy League endowment to enter.

On the other hand, Brevan Howard cut 17,700 $BTC, Harvard trimmed roughly 20%, and Royal Bank of Canada fully exited, all of which are mentioned in the CoinShares Q4 2025 report.

Aggregate pension fund and endowment crypto holdings peaked at $1.48 billion in Q3 2025, then declined to $965 million in Q4.

However, ETFs only reveal who is buying the wrapper. For those who are holding the asset itself, the balance sheets tell a different story.

Corporate Treasuries Show Who Holds Bitcoin Directly on the Balance Sheet

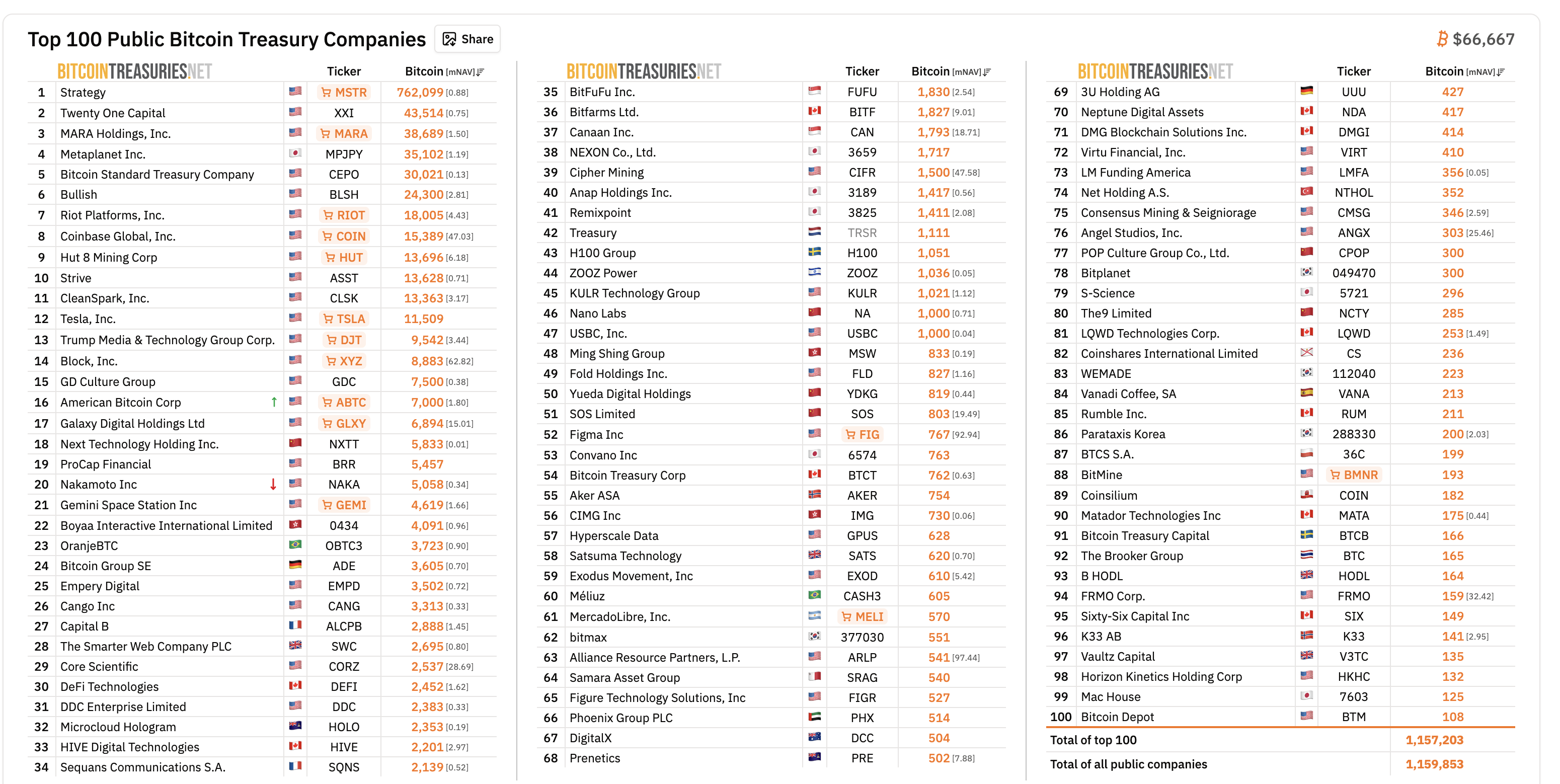

Beyond ETFs, a growing number of public companies hold Bitcoin directly as a treasury reserve asset. As of March 31, 2026, publicly traded companies report a combined 1,134,324 $BTC on their balance sheets.

The concentration is extreme. Strategy Inc, formerly MicroStrategy, held 762,000 $BTC as of April 2, 2026. Other big names in the space include Twenty One Capital, MARA Holdings, Japan’s Metaplanet, and more.

New entrants are reshaping the picture. Trump Media (DJT) held 11,542 $BTC before pledging 2,000 $BTC as collateral under a hedge arrangement with rehypothecation rights, reducing on-balance-sheet holdings to 9,542 $BTC. MARA sold 15,133 $BTC in March 2026 at a loss to service debt.

🚨 Arkham Analyst Corrects: Trump Media Didn't Sell 2000 $BTC, It Was Transferred as Collateral

— 0xzx (@0xzxcom) February 28, 2026

Arkham analyst Emmett Gallic has corrected his previous statement regarding Trump Media & Technology Group (TMTG) selling 2000 $BTC. Gallic has deleted the original tweet and clarified…

Yet corporate treasuries only account for direct spot ownership. Wall Street’s largest players are building crypto exposure through an entirely different mechanism, one that does not require holding a single Bitcoin.

Tokenized Funds and RWA Holdings Show Where On-Chain Meets TradFi

Some of Wall Street’s largest firms now build crypto exposure without holding a single token. Instead, they put traditional assets on-chain through tokenization.

BlackRock’s BUIDL fund, a tokenized US Treasury money market product, reached $2.85 billion in total assets ($2.17 billion at press time).

In February 2026, BlackRock began trading BUIDL on Uniswap’s decentralized exchange and purchased UNI governance tokens. That marked its first direct engagement with DeFi trading infrastructure.

The firm’s 2026 chairman’s letter reported $65 billion in stablecoin reserves, $80 billion in digital-asset ETPs, and nearly $150 billion in total digital asset-linked AUM.

The broader market is scaling fast. RWA.xyz data as of April 2026 shows $12.67 billion in on-chain US Treasury debt, representing roughly 46% of the total $27.59 billion in tokenized real-world assets.

That total RWA figure grew 31.61% in just the last 30 days alone, with 708,377 asset holders across the ecosystem.

This is Wall Street holding crypto infrastructure, not crypto assets. However, all of it depends on one thing. Who has the keys.

The Custody Map Reveals a Single Point of Failure

Knowing who owns Wall Street’s crypto is only half the picture. The other half is who holds the keys.

Coinbase custodies over 80% of US Bitcoin and Ethereum ETF assets, a figure confirmed by CEO Brian Armstrong. Coinbase was the custodian for eight of the 11 spot Bitcoin ETF listings at launch. Only Fidelity self-custodies its own fund. VanEck selected Gemini.

This concentration creates a single-cluster dependency. A cyber incident, service disruption, or governance failure at one custodian could affect multiple funds simultaneously, with knock-on effects for creations, redemptions, and trading liquidity.

On the tokenized side, Bank of New York Mellon serves as BUIDL’s cash and securities custodian, while Anchorage Digital, BitGo, Copper, and Fireblocks support BUIDL subscribers.

As of March 2026, discussions are emerging around multi-party computation custody and multi-custodian mandates to spread risk. No structural changes have materialized yet.

The custody map reveals a paradox at the heart of Wall Street’s crypto exposure. A decentralized asset class funneled through increasingly centralized infrastructure. And that infrastructure still leaves major holders invisible, specifically those with no filing obligation at all.

The Shadow Holders and What No Filing Can Show

13F filings only apply to US institutional managers with over $100 million in qualifying assets. Family offices, offshore entities, and sovereign vehicles operating through intermediaries are not subject to disclosure obligations.

That creates a structural blind spot in Wall Street’s map of crypto ownership.

On-chain data reveals what filings cannot.

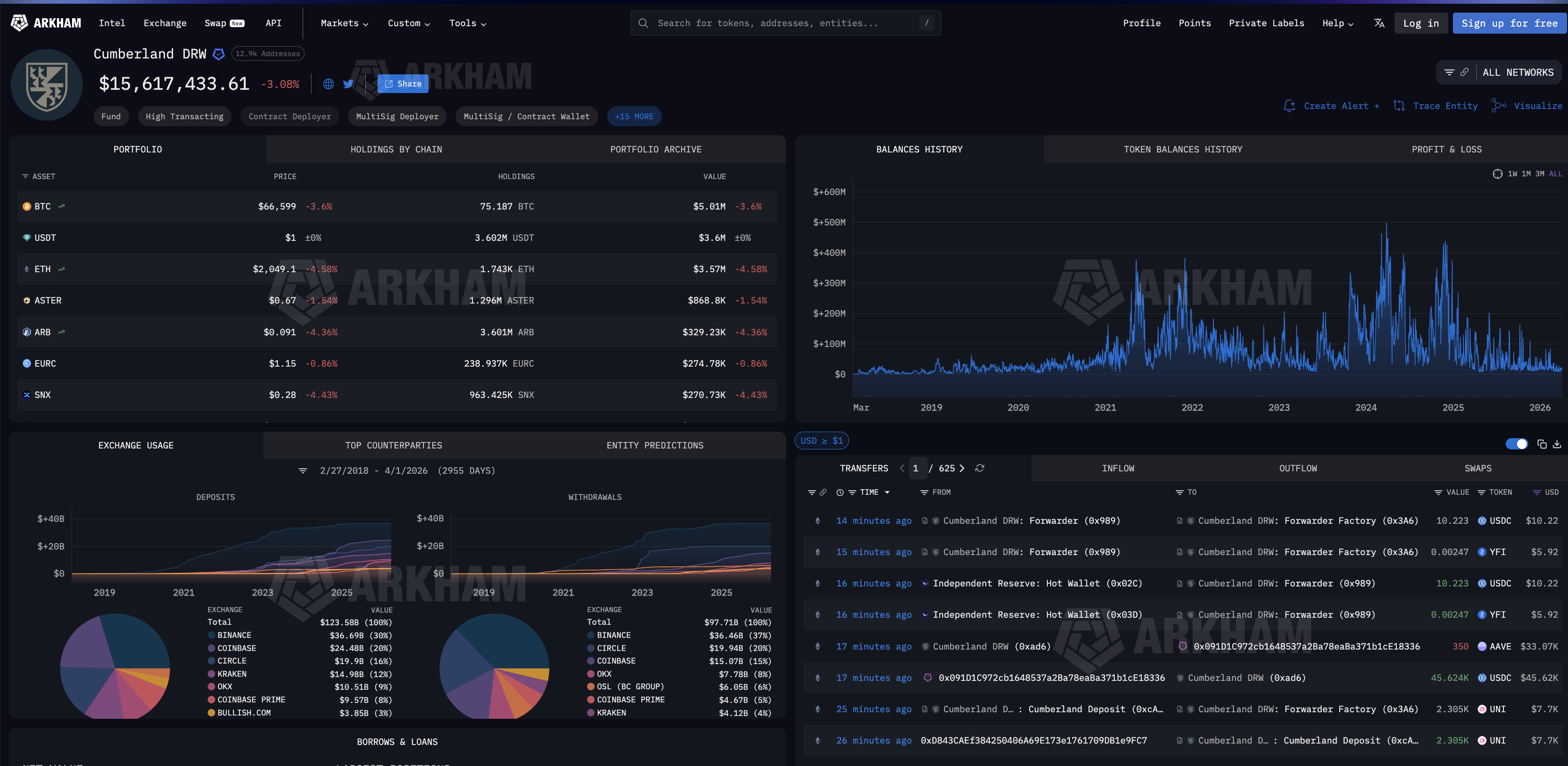

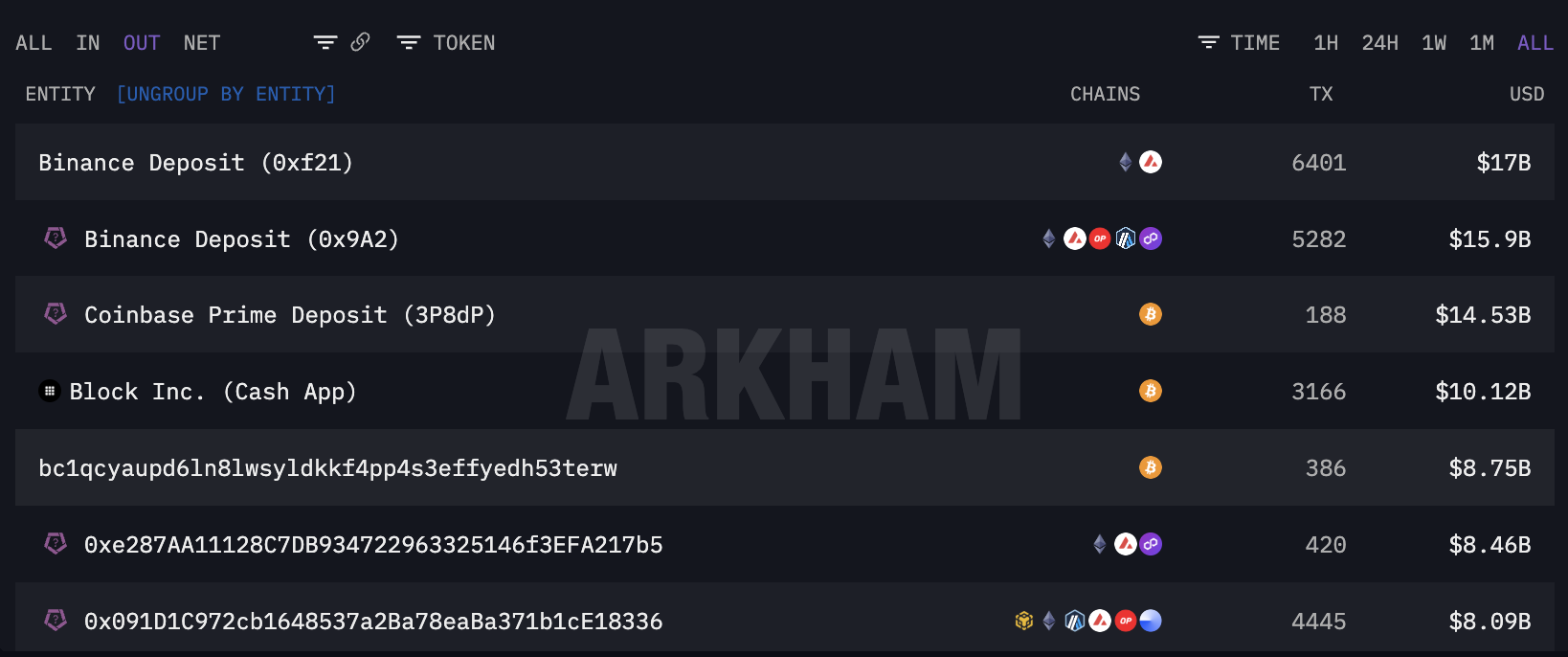

Cumberland DRW, one of Wall Street’s primary OTC desks, has processed a total of $123.58 billion in deposits and $97.71 billion in withdrawals across major exchanges since 2018.

Filtering Cumberland’s outflows reveals where institutional capital actually goes. The top all-time outflow destinations include $17 billion to Binance, $14.53 billion to Coinbase Prime, likely for ETF creations, and $10.12 billion to Block Inc..

Scrolling further down the counterparty list confirms additional ETF and institutional plumbing. Fidelity’s FBTC ETF inflows appear at $7.28 billion across 171 transactions.

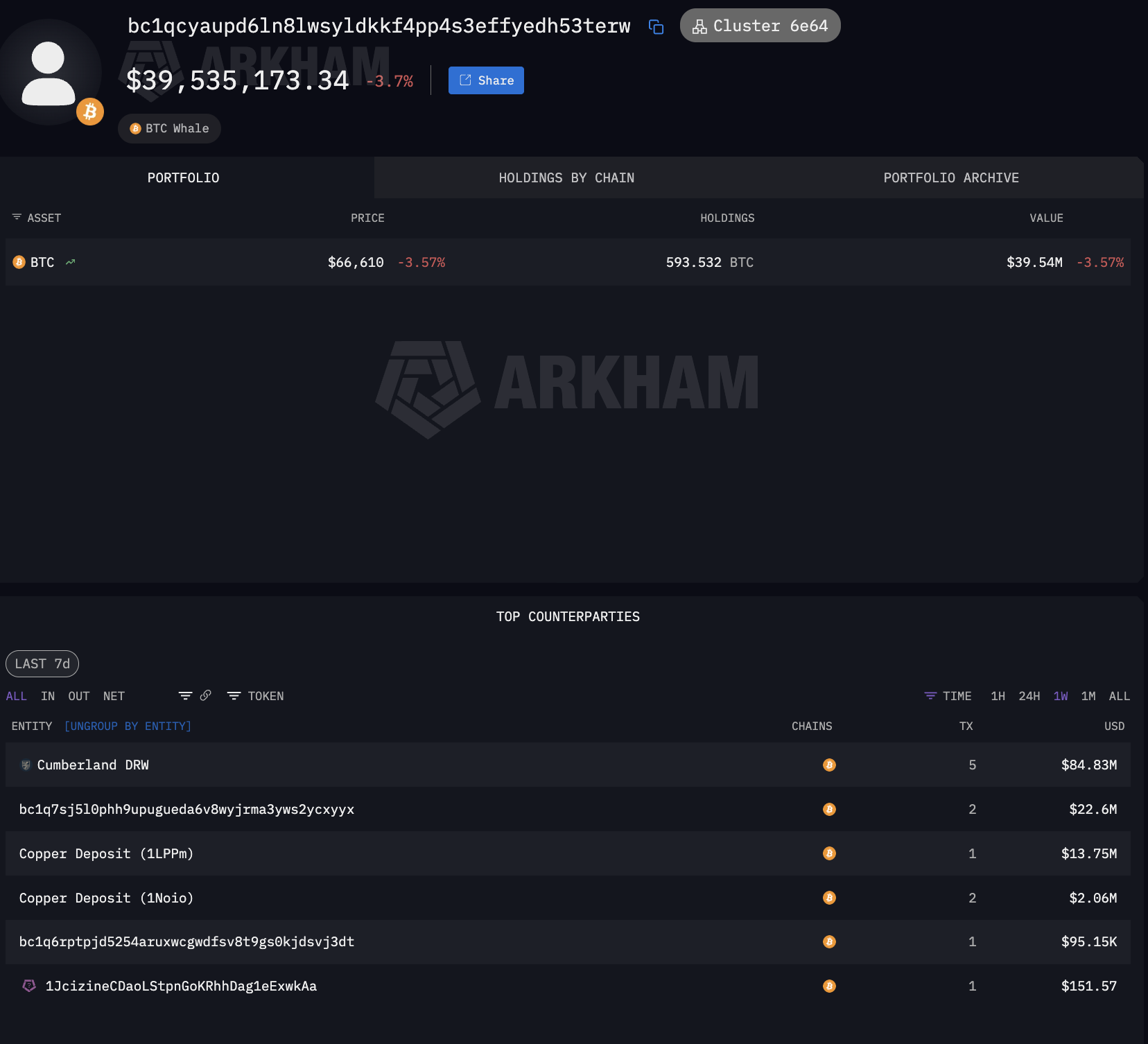

Alongside these labeled flows sit billions more directed to unlabeled wallets. The single largest unlabeled $BTC recipient, wallet bc1qcyau..., received $8.75 billion across 386 transactions.

It currently holds 593 $BTC and uses Copper’s institutional prime brokerage for custody.

That pattern, large OTC sourcing through a Wall Street trading firm paired with institutional-grade prime brokerage custody, is exactly the profile of a family office or sovereign vehicle operating through the same infrastructure as ETF issuers, just without the filing obligation.

The filings show part of the answer. The chain shows the rest.

The gap between the two hides durable demand from shadow holders who bought through a drawdown and still hold through institutional custody, suggesting deeper structural support than any ETF tracker captures.

That same gap also hides an untracked concentration that could crack it.