12

12

The era of buying bitcoin and calling it a treasury strategy is over.

By early 2026, more than 200 publicly listed companies hold digital assets on their balance sheets, collectively managing over $115 billion (DLA Piper, October 2025). The total market capitalization of these companies reached approximately $150 billion by September 2025 – a nearly fourfold increase from the year before. Yet several of these companies now trade at discounts to the value of the assets they hold. The market is sending a clear signal: accumulation alone is no longer enough.

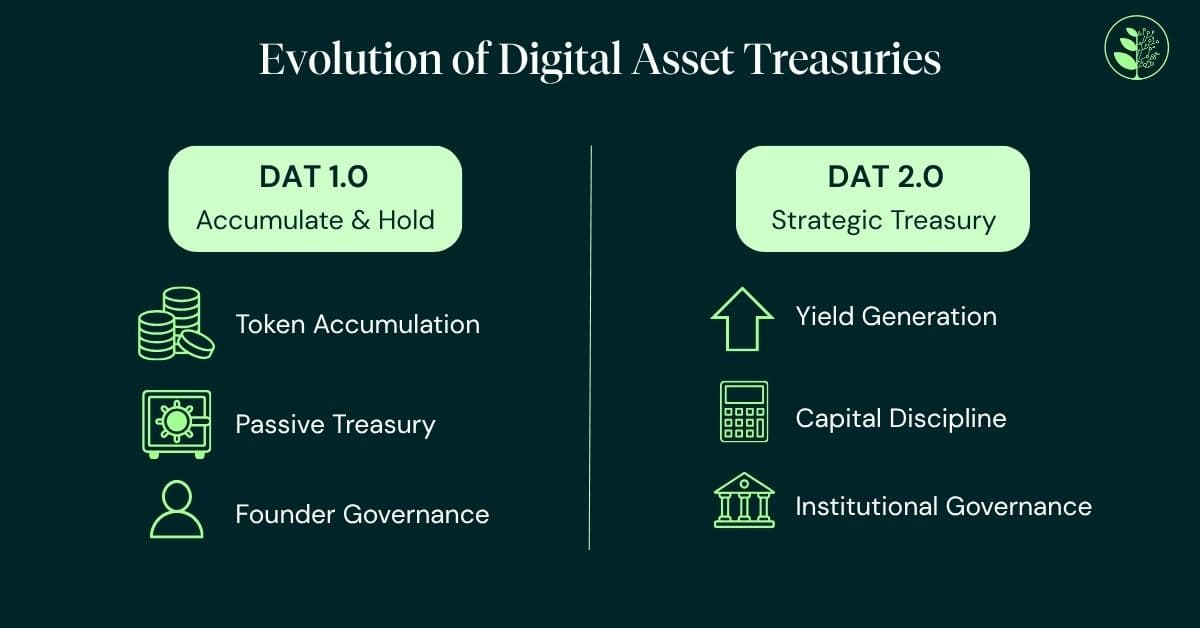

Investors want to see capital discipline and economic return. Management teams have responded with share repurchase programs and transparency metrics such as “$BTC per share,” designed to show the value a treasury adds beyond the token price (AMINA Bank Research, 2026). The shift from passive accumulation to active yield generation – from “DAT 1.0” to “DAT 2.0”—is now the defining theme of the sector.

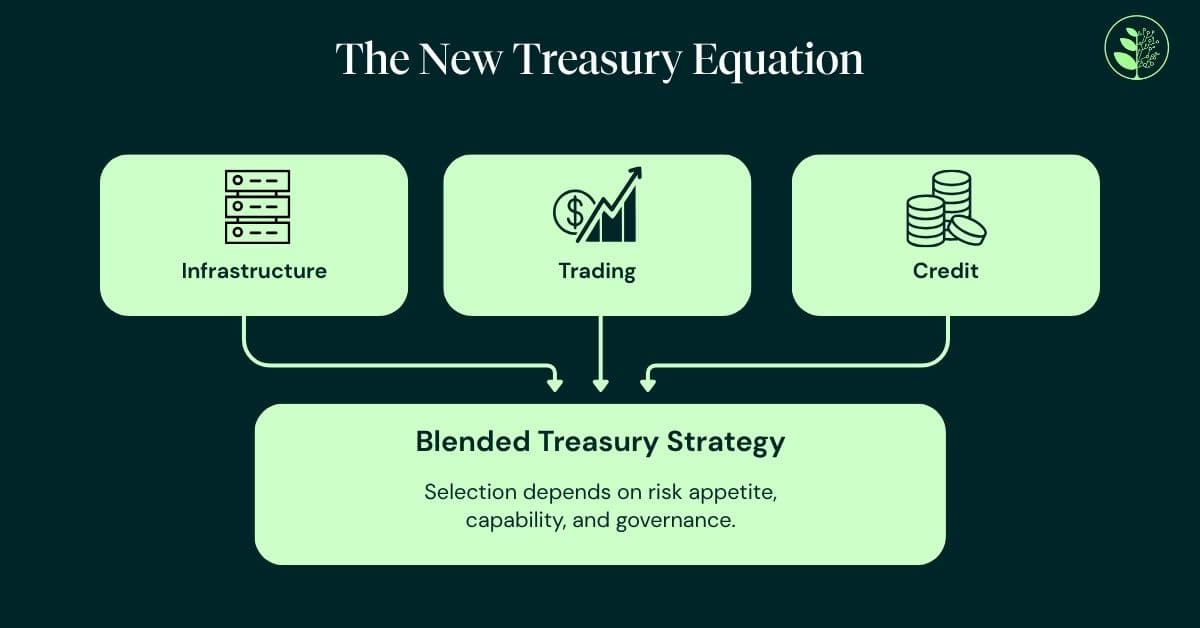

Three broad models are emerging. Each carries a different risk – return profile and places distinct demands on governance, technical capability and infrastructure.

Infrastructure participation and staking

The most protocol-native approach involves staking tokens to support network consensus and earning rewards in return. For bitcoin-focused treasuries, this increasingly extends to the Lightning Network and other native infrastructure that generates routing and liquidity-based fees. Staking requires careful analysis of the technical security and smart contract risks.

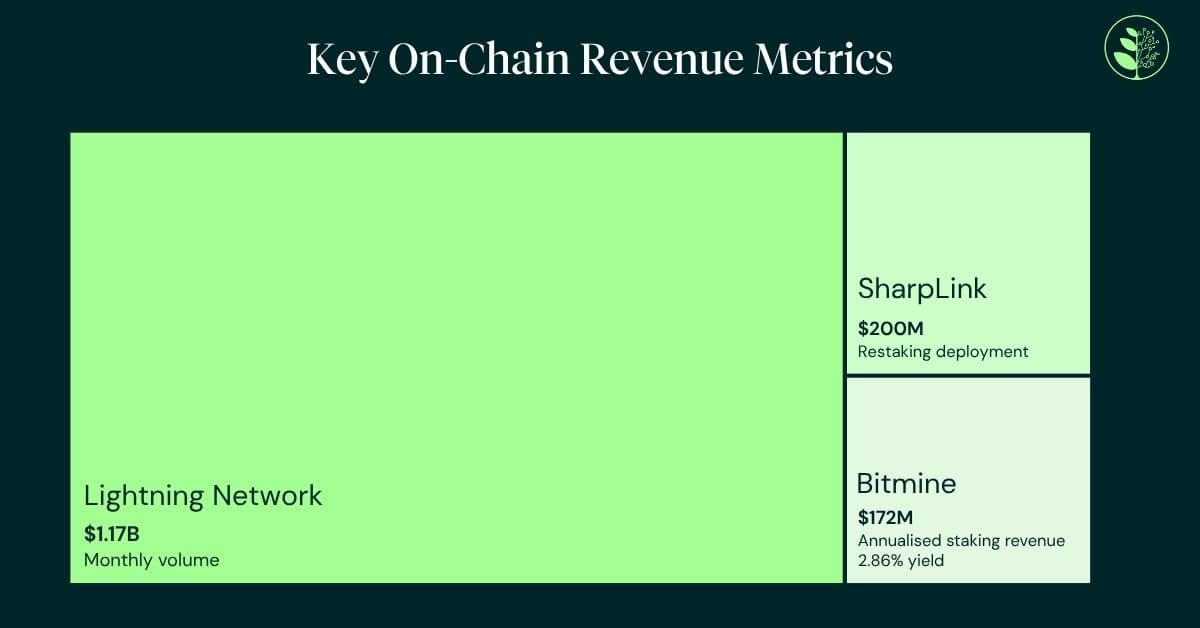

The numbers have grown quickly. Bitmine Immersion Technologies reported over 3 million staked $ETH by early 2026, with total holdings of $9.9 billion and annualized staking revenue of approximately $172 million (SEC Filing, March 2026). Its proprietary validator network marginally outperformed the Composite Ethereum Staking Rate, demonstrating the edge that institutional-grade infrastructure can deliver even in a protocol-level yield environment.

SharpLink Gaming deployed $200 million in $ETH into restaking infrastructure via EigenCloud, targeting higher yields by securing applications ranging from AI workloads to identity verification (SEC Filing, 2025). Restaking – where already-staked $ETH is used to secure additional services, with careful governance.

Active trading and market-driven income

A second set of strategies leverages market structure – funding-rate arbitrage, basis trading and options premiums. These can be effective and often market-neutral, but they demand trading expertise, robust risk controls and round-the-clock monitoring. The governance implications are significant: this approach effectively converts a treasury function into a trading operation. Like any trading function, it can be difficult to find skilled staff required to monitor complex positions and correlation risks.

One prominent Japanese listed company illustrates both the potential and the complexity. Holding over 35,000 $BTC by the end of 2025, it generated the equivalent of approximately $55 million in bitcoin income revenue through option-based strategies, with operating profit growth exceeding 1,600% year-on-year. Yet the same company recorded a substantial net loss due to non-cash mark-to-market revaluations under local accounting standards (TradingView; Kavout, 2026). For investors, this disconnect between operational cash flow and reported earnings makes evaluation materially harder – and underscores why governance and transparency matter as much as headline returns.

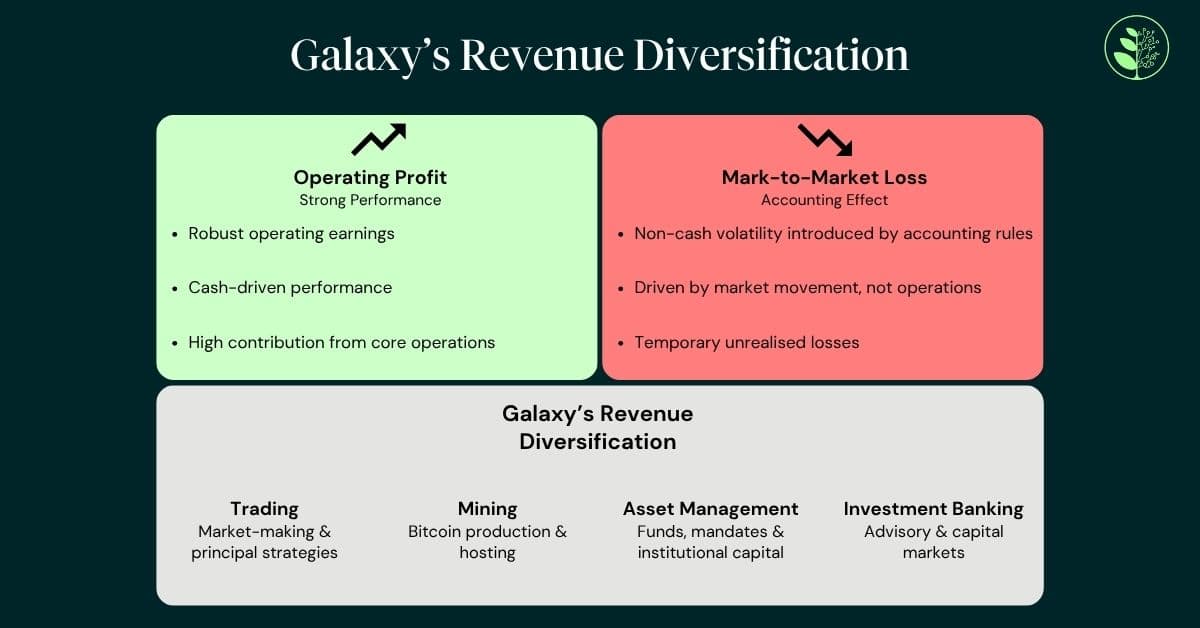

Galaxy Digital offers a contrasting hybrid model, combining its own digital asset treasury with institutional services including collateralized lending, strategic advisory, and infrastructure. In Q3 2025, Galaxy posted a record adjusted gross profit of over $730 million (Mint Ventures Research, 2025). Notably, the firm has diversified its yield sources beyond pure crypto by repurposing its Helios mining facility as an AI compute campus secured by long-term contracts – a signal that the most resilient treasuries may be those that derive income from multiple, uncorrelated sources.

Credit deployment and net interest margin

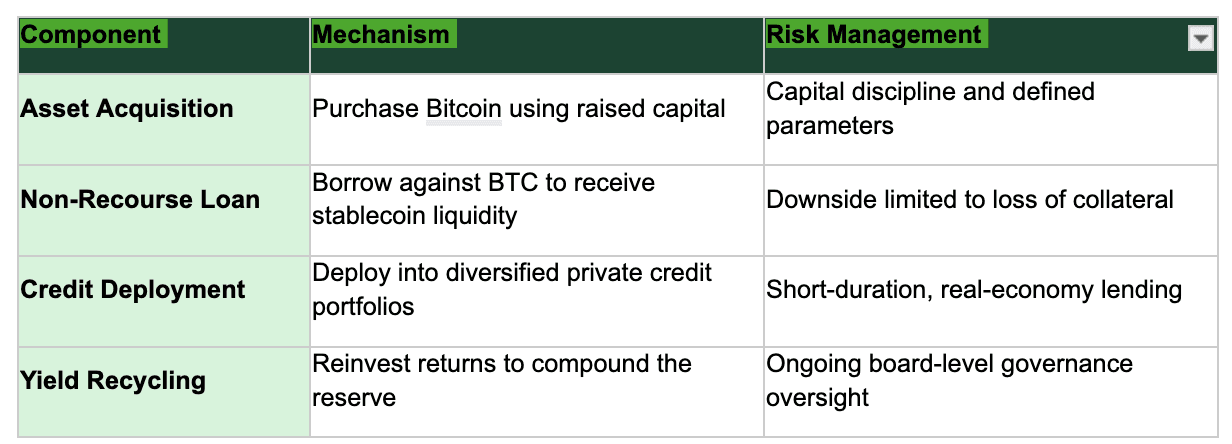

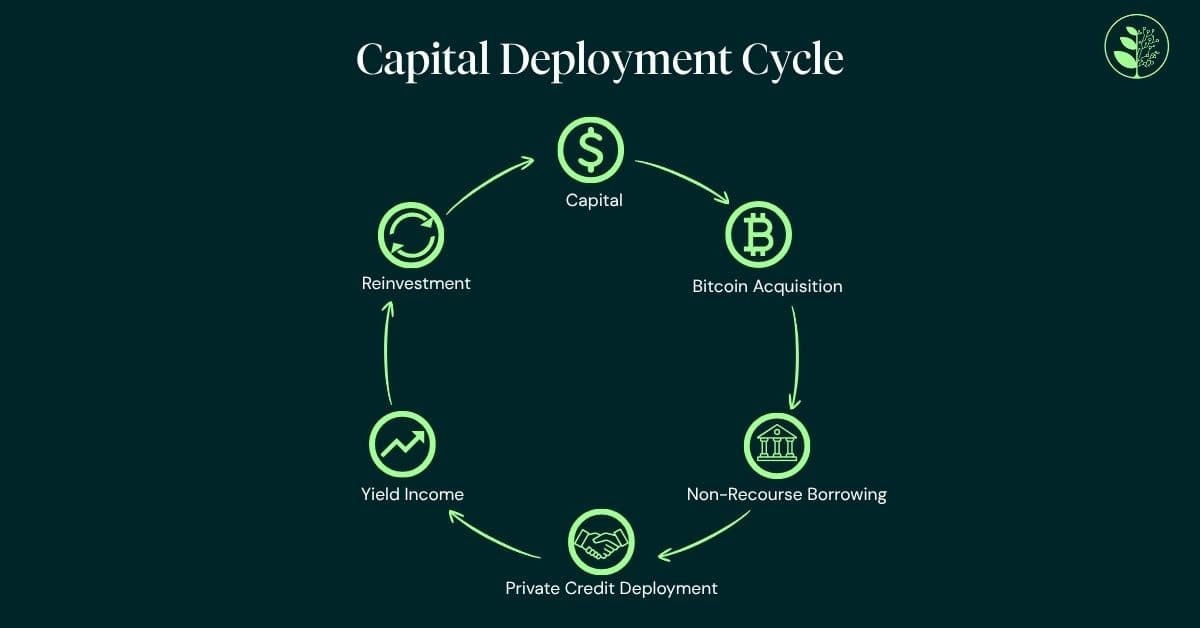

A third route treats digital assets as productive balance-sheet capital. The model involves borrowing against crypto holdings on a non-recourse basis, receiving stablecoin liquidity, and deploying it into higher-yielding private credit. It preserves long-term exposure to the underlying asset while generating recurring interest income from short-duration, real-economy lending. In particular, this strategy demands expertise in yield, credit risk and fixed income.

The mechanics draw directly from traditional banking: liquidity management, underwriting, governance and controlled leverage. Under this type of model, a company acquires bitcoin, borrows against those holdings on a non-recourse basis—meaning the downside is limited to the collateral—and deploys the proceeds into diversified private credit portfolios supporting real-economy lending. If bitcoin appreciates, the company retains the upside after repaying the loan, combining potential capital gains with recurring interest income.

For credit deployment models to work credibly, they need to be grounded in operational financial infrastructure rather than built from scratch. The approach is most effective when it extends from an existing platform with real lending relationships and established client accounts. In our view at Greenage, this is also an area where governance and due diligence frameworks are particularly important, given that capital is being deployed into third-party credit opportunities that must be assessed on a counterparty-by-counterparty basis.

The success of this model is also tied to the maturation of stablecoins as institutional infrastructure. By 2026, stablecoins underpin cross-border payments, real-time settlement and T+0 clearing (same-day settlement) for enterprises (Foley & Lardner, January 2026). Coinbase Institutional projects total stablecoin market capitalization could reach $1.2 trillion by 2028 (Coinbase Institutional, August 2025). For credit deployment strategies, stablecoins provide a sound medium for capital deployment in lending markets.

The new measure of maturity

Recent market conditions have reinforced a simple truth: price appreciation alone is not a treasury strategy. The growing range of yield solutions reflects a sector learning from its own history—sustainable income generation makes digital assets more productive components of a corporate balance sheet.

No single model is definitive. The most effective treasuries will blend approaches depending on risk appetite, operational capability and governance structure. But the direction of travel is clear. Passive holding is no longer sufficient to justify digital assets’ place on the balance sheet. Yield is becoming the central measure of treasury maturity –and the core factor in how the market values companies with digital asset exposure.

The winners in this next phase will not be the largest holders. They will be the most disciplined operators.

Important Notice:

This article has been prepared by Greengage & Co. Limited for informational and thought leadership purposes only. It is intended solely for use by businesses, professional counterparties and institutional market participants and is not directed at retail consumers. It does not constitute financial advice, investment advice, a financial promotion, or a recommendation or inducement to buy, sell, or hold any asset, security, or financial instrument.

Digital assets are subject to significant price volatility and regulatory change. Past performance is not indicative of future results. All investments carry risk, including the potential loss of capital. Forward-looking statements and market projections referenced herein are sourced from third-party research and do not represent the views or predictions of Greengage & Co. Limited.

Greengage & Co. Limited is not authorized or regulated by the Financial Conduct Authority for investment business. Greengage acts solely as an introducer to independent third-party service providers and does not arrange investments, provide lending, custody, or investment management services.

Readers should seek independent professional advice before making any investment decision.