1

1

When the net present value of Stretch (STRC), the dividend-yielding preferred share issued by Strategy (formerly MicroStrategy), is calculated, it makes disappointing reading for MSTR shareholders.

Michael Saylor hopes that STRC will somehow fund trillions of dollars worth of bitcoin ($BTC) purchases for shareholders of his common stock. However, while STRC raises capital that will mathematically create a positive $BTC yield for MSTR, it’s actually extraordinarily expensive over the long term.

Strategy advertises these immediate $BTC purchases as the up-front benefit of STRC to its MSTR common stockholders.

It happily praises $BTC Yield, the extra quantity of $BTC that MSTR shareholders enjoy today when Strategy buys $BTC from the cash it receives selling STRC.

STRC obviously improves the company’s current balance sheet because it raises capital today and throws all of its servicing costs into the future. Like any other capital-raising activity, Strategy promises future benefits in exchange for capital today.

Read more: Michael Saylor’s Spinal Tap ad says STRC is like a bank account — it isn’t

The 11.5% dividend

Despite STRC’s morphing terms, such as its variable interest rate and quasi-peg, it’s possible to estimate what STRC is worth today.

Although no one has offered to buy out STRC from Strategy entirely, a theoretical calculation about what this asset is worth can illustrate its actual value for common shareholders of the company, rather than the misleading $BTC yield metric that ignores all of STRC’s future obligations.

Specifically, STRC pays 11.5% annualized dividends in monthly cash installments.

Although its dividend rate is variable and subject to suspension at the discretion of the board of directors, a prospective buyer could use 11.5% as a rate for calculation.

Indeed, if STRC trades substantially below its $100 par value (also called its “stated amount”) in the future, as it has in the past, the company might need to increase that percentage further to encourage bids from Nasdaq traders.

It could also lower that rate if STRC trades far above its $100 stated amount.

In essence, using the 11.5% dividend rate, as-is, is a fair starting point for calculations. The rate is the company’s current choice, and the market is pricing STRC based on that dividend at this time.

Worthwhile to compare STRC to a junk bond?

Assuming a bond portfolio buyer were interested in STRC, they might compare its dividend interest rate to an average junk bond yield. Indeed, Strategy itself has a junk “B-” creditworthiness rating by S&P.

Saylor has repeatedly compared STRC to a high-yield bank account or money market fund, even though it has no deposit insurance, doesn’t have any guarantees to maintain principal value, doesn’t pay any guaranteed interest rate, has no standing bids in the market to support secondary trading at par, and has fluctuated in value by 9.8% over the last four months.

Still, many crypto investors have learned about high-yield bonds for the first time by way of STRC’s retail-focused advertisements, including various X ads and a Spinal Tap appropriation that claim its dividends are somehow “income” that can “stretch” a typical 3-4% money market interest rate payout to 11.5%.

Even though STRC isn’t a bond, its marketing promises are very similar to a bond offer, emphasizing monthly payouts, an annualized interest rate, and a vague insinuation that the principal of the investment might remain stable in value.

It has vast documentation about Strategy’s attempts to pull financial levers if STRC trades too far above or below its $100 par.

Of course, a company paying 11.5% to raise capital is a red flag in itself. Investment grade corporate bonds pay about 5%. Even the most risky, Baa-rated companies with creditworthiness just one step above junk status pay an average 6.1%.

An 11.5% rate is far higher than even junk bond rates, which average near 7%.

Indeed, the 7% average junk bond yield is a starting point for calculating and then doubting one’s calculations about the net present value of STRC in comparison to a junk bond portfolio.

With a massive, 450 basis point credit spread above the average junk yield yet with no principal repayment and no maturity date, STRC’s 11.5% dividend is so high that it seems to be more like an annuity than a bond.

Calculating STRC like an annuity

Annuities, in contrast to bonds, can be structured to pay almost any annualized interest rate… if the pay term is short enough. Give an annuity company $1 million and ask for a 10% simple interest for only 10 years, and they’ll happily oblige.

That is free money for the annuity company, paying back only the principal while enjoying investment yields on the balance for a decade.

Indeed, because STRC is a choose-your-own adventure product by Strategy which plucked the 11.5% dividend rate out of its discretion, it’s far more comparable to a custom annuity than a bond.

There is, in addition, a well-established and relatively liquid market for annuity settlements.

Annuity settlements provide a reference point for a one-time cash payout for an instrument that never repays its principal or matures. Although STRC might theoretically pay dividends for centuries, limiting its payouts to the lifetime of a human, like Saylor, is probably a more realistic starting point than infinity.

An annuity-style cash settlement estimate of STRC would then have to be compared against the value of another annuity paying the average yield of a junk bond, i.e. 7%, and discounted against the value of the bond’s principal repayment upon maturity.

Unlike bonds, classic income annuities don’t typically repay principal at any date. Instead, like STRC, they irreversibly convert a principal capital into a payment stream over the lifetime of the policyholder.

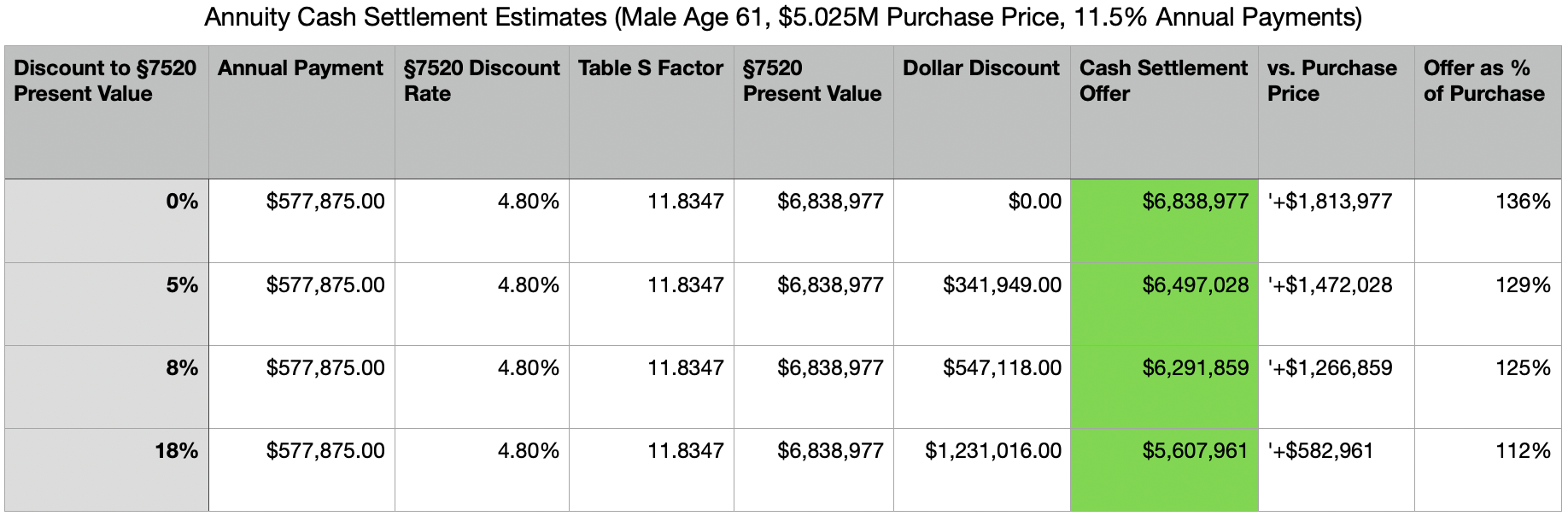

What is a $5 billion annuity paying 11.5% worth?

If you plug a $5.025 million classic life-only annuity into an actuarial calculator paying 11.5% annually until death of a 61-year-old US male policyholder, i.e. the same age as Saylor, the likely cash settlement offer for a one-time buyout of this annuity ranges from an aggressively lowballed, 18% discount bid of $5.6 million to a more realistic, fair market discount of 8% at $6.3 million.

Simply substitute the word million for billion, above, to translate that into the net present value of STRC’s $5.025 billion in notional outstanding.

Of course, STRC isn’t legally tied to anyone’s lifespan and dividends can, in principle, run indefinitely or be cut earlier.

Using Saylor’s life to cap the horizon is a simplifying assumption, not an inherent property of STRC.

Yes, this theoretical $5.025 million annuity immediately gains value in a cash settlement here because the generous, 11.5% yield rate instantly accrues value in the secondary market for the obvious reason that such payouts are not generally available elsewhere from creditworthy issuers.

Discounts like 8% or 18%, above, are calculated based on the mathematical value of an annuity, defined by IRS publication 1457, also known as a Section 7520 valuation.

For a level-paying annuity under §7520, its present value calculates using a §7520 rate and the appropriate mortality table.

In plain English, the net present value, or the whole stream of future payments as valued right now in today’s dollars, equals the dollar amount of each payment in the annuity multiplied by an IRS-defined annuity factor that provides the discount rate and mortality assumption based on age and gender.

The practical negotiating range is roughly $6 million, corresponding to the 5-10% discount rate band that dominates the annuity “settlements” bids.

A well-negotiated deal with multiple competing bids could push closer to $7 million, since the 11.5% interest rate is exceptionally rich relative to current market rates and buyers would have a strong incentive to compete.

The fair value floor is actually above principal, or above $6 million, because 11.5% annual cash yield against a 6-7% average cost of capital for an institutional buyer elsewhere creates an immediate positive carry rate from day one.

Any offer below $6 million would likely be predatory at a discount rate exceeding 18% that would primarily benefit the buyer at an unreasonable penalty to the seller.

So, despite STRC’s lack of any promise to repay principal, the discounted net present value of its future cash flows at 11.5% during Saylor’s expected life expectancy are probably worth something around $6-7 billion, or above the full value of its $5.025 billion notional of face value outstanding.

Again, when transposing figures from a realistic annuity measured in the millions, simply substitute the word billions to analogize to STRC.

Additional considerations

Of course, the buyer and seller in this hypothetical scenario could debate how much STRC’s dividend rate will vary, because it is a variable rate, after all.

Moreover, they could debate whether STRC will maintain its $100 par value on the secondary market, i.e. on its Nasdaq listing.

If any buyer was somehow 100% confident that STRC would maintain its $100 par by the end of Saylor’s lifetime, they might bid double that $5 million par or more, i.e. $10-12 billion, for the entire STRC product today.

Of course, no one is actually bidding over $200 for STRC today, as it hugs its quasi-peg closely at $99.75 as of writing time.

Therefore, the market somewhat agrees with the annuities comparison above. However, it discounts the comparison with little faith in the long-term ability of STRC to maintain its $100 quasi-peg.

The discounted net present value of STRC’s future cash flows, if it were to actually pay 11.5% annualized dividends over the course of Saylor’s lifetime, is actually worth at least $1 billion more than its $5.025 billion face value. If the bidder had confidence that STRC would still hold its par value on the Nasdaq by the end of Saylor’s life, it should be worth more than double the current $100 share price.

So how, exactly, does Strategy expect a product that’s worth so much less than the cash settlement value of its comparable peer, an annuity, to make up for that lack of confidence while also making good on all of those future payouts?

The market has spoken, giving STRC no more value today at its $5.012 billion market capitalization than its $5.024 billion face value on which it raised money to buy $BTC.

The only way this works is if $BTC rallies. A lot.

For the STRC trade to work for Strategy, $BTC has to rally much more than 11.5% annually.

If only $BTC were to rally 30% a year, it would pay for everything

As usual, STRC’s lavishly generous dividend of 11.5% only makes sense if $BTC appreciates far above that rate. It could, for example, rally along the lines of Saylor’s hyper-bullish forecast of 30% per year.

Obviously, selling something paying 11.5% to buy something appreciating 30% is a no-brainer, as long as that thing actually appreciates 30% annually.

Unfortunately, for the last five years, $BTC definitely hasn’t rallied anywhere close to 30% per year. Instead, it’s only rallied 30% in five years.

In Saylor’s mind, $BTC will soon make up for those shortcomings.

It better. All of Strategy’s $BTC-acquiring efforts have lost money on average, so Saylor needs $BTC to rally desperately. The company’s average cost basis is $75,696 or 5% higher than $BTC was trading today.

In summary, the result of both an annuities-style cash settlement value valuation of STRC, as well as the real market capitalization of STRC, both align with a value at or above STRC’s face value on which it raised money to buy $BTC: $5 billion.

However, because STRC is actually trading at a market cap equal to its face value, the market is giving Strategy shareholders no more benefit today for STRC than the initial capital that it has raised over the last year to buy $BTC.

There might be $BTC yield per share of MSTR, but MSTR isn’t enjoying any benefit from STRC as measured in USD.

Worse, the company has to pay dividends to STRC indefinitely, even though the market is giving STRC no benefit above par for that promise today.

Those future obligations will drag on the company’s profitability and cash flows for years to come.