6

6

Coinbase just dropped a grenade on Wall Street. The company missed big, reporting Q4 revenue of $1.78 billion, down 31%, and an earnings per share (EPS) of -$2.49.

Analysts had expected a profit of $0.96 per share. Instead, the company posted a massive net loss of $667 million. This was not a small miss. It was a full-on disaster.

Revenue fell across the board. Transaction revenue sank to $983 million, down 6% from the previous quarter. Subscription and services revenue dropped 3%, ending at $727 million. Expenses didn’t follow the same direction.

Coinbase’s operating costs actually went up 9%, hitting $1.5 billion. Coinbase’s spending on tech, admin, and sales grew 14% to $1.3 billion. The company also increased its full-time staff by 3%, ending 2025 with 4,951 employees.

Institutional trading lifts but consumer volumes tumble

Consumer trading did not help. Coinbase’s consumer spot trading volume fell to $56 billion, a 6% drop, and revenue from that dropped 13% to $734 million. The company blamed this on a shift from “simple” to “advanced” trades and growing use of the Coinbase One plan, which offers discounted fees. That’s the kind of trend that might feel good for users, but it hurts the bottom line.

On the institutional side, spot trading volume fell 13% to $215 billion, but revenue jumped 37% to $185 million thanks to derivative trading, especially through Deribit. CEO Brian Armstrong said, “We saw strength in institutional derivatives during the quarter, despite lower spot volumes.”

Despite the bloodbath in Q4, Coinbase’s full-year transaction revenue for 2025 totaled $4.1 billion, up 2% year-over-year. That came from $3.3 billion in consumer, $479 million in institutional, and $252 million in other transaction revenue.

Stablecoin activity hits new highs despite interest rate cuts

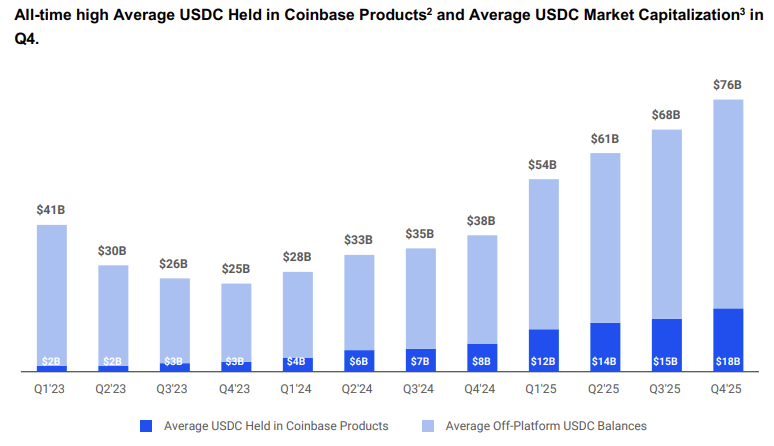

Not everything fell. Stablecoin revenue was up 3%, reaching $364 million in Q4. Coinbase said the average $USDC held in its products rose 18% to $17.8 billion, a record high.

Average off-platform $USDC balances also went up 11% to $58.4 billion. The company said, “We believe Coinbase continues to be one of the best places to use stablecoins.”

Still, interest income got hit. Q4 interest and finance fee revenue dropped 8% to $60 million, mostly due to falling interest rates after cuts in October and December. Despite this, Coinbase’s institutional loan book hit an all-time high in daily average balances of $1.3 billion, with $1.4 billion in collateralized loans issued to clients, including Bitcoin miners.

On blockchain rewards, revenue dropped hard, down 18% to $152 million. ETH and SOL prices fell 13% and 16%, dragging down staking returns.

Also, Solana’s protocol reward rate declined 17%, though Coinbase did report higher staking volumes. Custodial fees were another weak spot, falling double digits due to lower crypto prices.

Coinbase One subscribers hit new record but earnings still bleed

Coinbase One, the firm’s subscription service, helped boost some numbers. Q4 subscription and services revenue included $152 million from other sources, up 6% quarter-over-quarter.

This included Coinbase One fees and rewards, which grew sharply. The number of paid Coinbase One subscribers hit 971,000, nearly four times higher than two years ago. The service now includes perks like a Coinbase One Card with up to 4% back in Bitcoin, and access to special offers like “Member Week”.

Brian Armstrong said, “Coinbase One continues to gain traction with both retail and institutional customers. We’re pleased with how adoption is growing.” The base plan costs $4.99/month, and Coinbase is betting that bundling services will boost long-term revenue.

Still, the cost of growth is showing. Stock-based compensation added about $250 million to the expense sheet for Q4.

Coinbase also spent $1.7 billion buying back its own stock during the quarter and through February 10, 2026. The company ended the year with $11.3 billion in cash and cash equivalents, which now includes payment stablecoins like $USDC.

Outlook shows weak guidance for Q1 2026 as risks continue

Looking forward, the numbers aren’t looking better. Coinbase said it had already generated about $420 million in transaction revenue through February 10, 2026, but warned not to read too much into that. Subscription and services revenue is projected between $550 million and $630 million for Q1 2026, down from the $727 million in Q4.

Spending levels are expected to stay flat. The company forecasts $925 million to $975 million in tech and admin costs, and $215 million to $315 million in marketing. Coinbase expects transaction expenses to stay in the low-to-mid teens range as a percentage of net revenue. Stock-based compensation will remain around $250 million, driven by more hires and recent acquisitions.

Coinbase said, “As always, we urge caution in extrapolating results early in the quarter.” But it didn’t offer much else to comfort anyone still holding onto the stock.

2025 may have been a big year for crypto markets, with the total market cap hitting $4 trillion, and total crypto trading volume rising 26% year-over-year, but Coinbase’s earnings report shows they didn’t walk away with much profit.

Coinbase’s total revenue for 2025 was $7.18 billion, up 9% from 2024.