This is a segment from The Breakdown newsletter. To read more editions, subscribe.

“The continuous rise of the debt-to-GDP ratio indicates that current policy is unsustainable.”

— Financial Report of the United States Government

There once was a happy time when Fed chairs felt free to lecture politicians on their irresponsible spending habits.

In 1990, for example, Alan Greenspan told Congress he would lower interest rates, but only if it cut the deficit.

In 1985, Paul Volcker even specified a number, telling Congress that the Fed’s “stable” monetary policy was contingent on Congress cutting about $50 billion from the federal budget deficit.

(Oh, for the days when $50 billion of federal debt wasn’t just a rounding error.)

In both cases, the Fed chairs were not-so-subtly threatening Congress and the White House with recession: That’s a nice economy you’ve got there. Would be a shame if something happened to it.

Now, however, it’s the other way around, with President Trump lecturing the Fed on interest rates.

In just the last few weeks, the president has opined that the fed funds rate is “AT LEAST 3 points too high,” insisted there is “no inflation” and mocked the Fed Chair as Jerome “Too Late” Powell.

This, too, is a shakedown: That’s some nice central-bank independence you’ve got there…

President Trump lobbied for lower interest rates during his first term as well. Like nearly every modern US president, he wanted the Fed to stimulate the economy.

This time, however, it’s about much more than that: Trump wants the Fed to finance the deficit.

The Trump vs. Powell showdown is ostensibly about the current level of interest rates (which the FOMC left unchanged today, presumably to the president’s displeasure).

But what the president has been threatening is “fiscal dominance” — the state of affairs when monetary policy is subordinated to the needs of government spending.

“Our Rate should be three points lower than they are saving us $1 trillion a year (as a Country),” the president recently wrote on Truth Social (in his signature style of random capitalization).

With repeated such statements, Mr. Trump has made history by being the first US president to explicitly call for fiscal dominance.

But he’s far from the first to acknowledge the possibility.

When Volcker and Greenspan threatened Congress with rate hikes, it brought the usually hidden link between monetary and fiscal policy out into the open.

It worked for them: Both Fed chairs had some success in using the threat of recession to get Congress to address its deficit spending, which is a hopeful precedent.

But that tactic seems unlikely to work this time.

Chair Powell has often warned about the risks of growing deficits, and even explained that higher deficits could mean higher long-term interest rates.

But it’s hard to imagine him making an explicit threat in the way Volcker and Greenspan did — perhaps because he knows he’s bargaining from a much weaker position.

In the 1980s, the most-feared effect of higher interest rates was recession, which the Fed was willing to risk in order to get Congress to change its free-spending ways.

Back then, lawmakers faced a ballooning defense budget and a stagnant economy, both of which seemed manageable.

At just 35% of GDP, the national debt seemed manageable too.

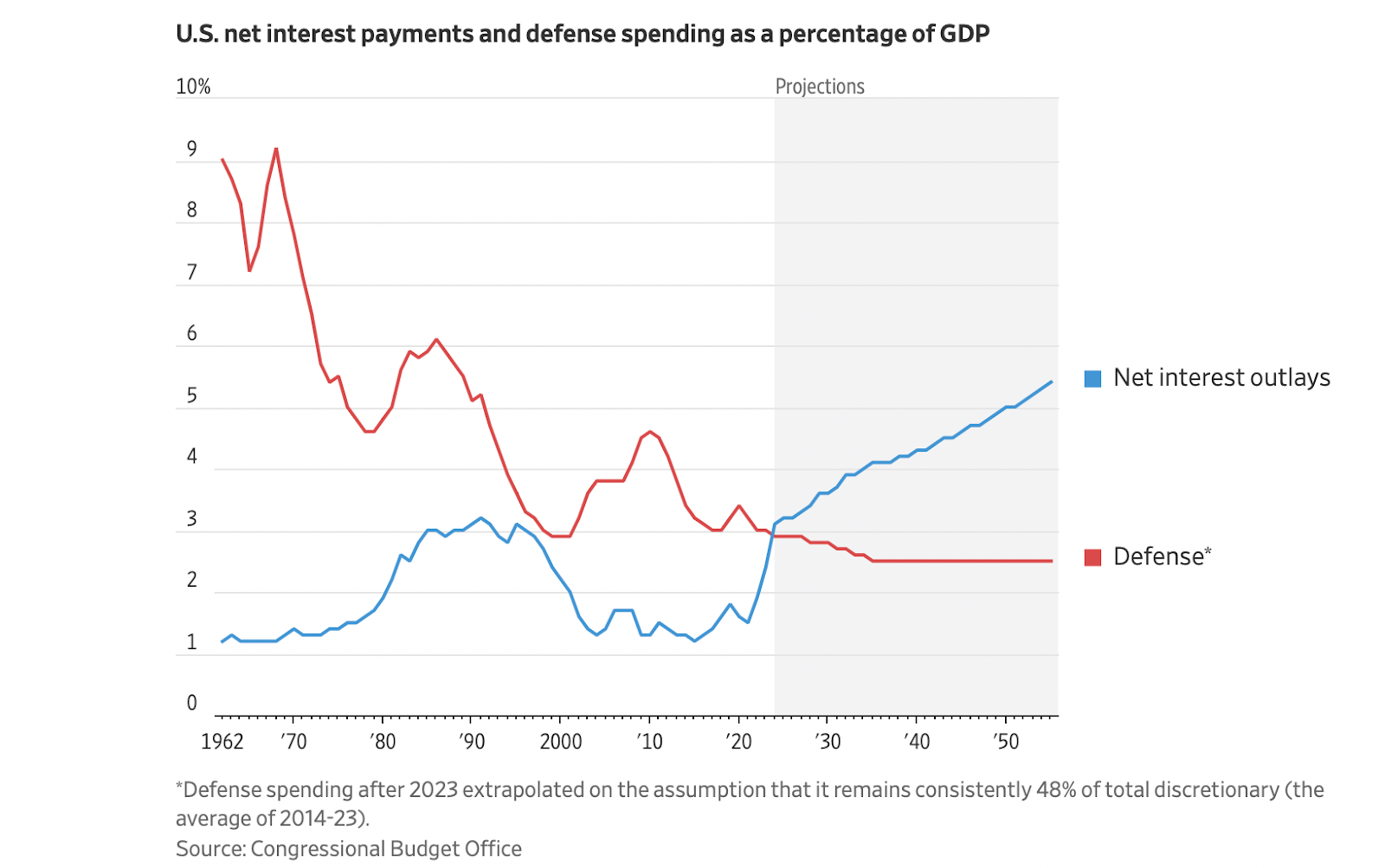

Now, with federal debt at 120% of GDP, the US spends more on interest payments than it does on defense:

The fast-rising blue line above may now be the biggest budgetary problem.

This puts the Fed in a bind because raising interest rates to encourage fiscal sanity would only exacerbate the problem it wants lawmakers to address.

The Fed could risk it, of course.

But if rate hikes drive the deficit even higher, who blinks first: the Fed or the White House?

Before answering, consider that 73% of federal spending is now non-discretionary, vs. just 45% in the 1980s.

To believe the Fed can win a showdown over deficits is to believe Congress will make significant cuts to non-discretionary spending like Social Security and Medicare.

This seems, well, unbelievable.

Now, especially, with a president who appears wholly unperturbed by the country’s growing indebtedness.

This may come from his experience as an over-indebted real estate developer in the 1990s.

“I figured it was the bank’s problem, not mine,” Trump later wrote of not being able to service his debts. “What the hell did I care? I actually told one bank, ‘I told you you shouldn’t have loaned me that money. I told you that goddamn deal was no good.'”

Now, as president, when Trump tells Powell that interest rates should be lower, what he’s really saying is that the national debt is the Fed’s problem, not his.

He’s not wrong.

“When interest payments on the debt rise and primary surpluses are politically off the table,” David Beckworth writes, “something else has to give. That something is more debt, more money creation, or both.”

Yes, the Fed could run the Volcker/Greenspan playbook and threaten Congress with higher interest rates.

But Powell presumably knows that following through would only exacerbate a problem that might ultimately be the Fed’s to fix — and pull forward the time by which it’s forced to fix it.

“If debt levels are too high and growing,” Beckworth explains, “it becomes the Fed’s job to accommodate — by suppressing interest rates or monetizing debt.”

That, and not President Trump, he warns, is the real existential threat to the Fed: “When the central bank is forced to accommodate fiscal needs, it loses its economic independence.”

Beckworth remains hopeful that it might not come to that.

And maybe it won’t. We’ve just seen how unpopular inflation is, so maybe if we get another bout of it, voters will force lawmakers to address the deficit.

But he despairs that the focus on Trump’s demands for lower interest rates is a distraction: “What we are witnessing is less about Trump himself and more about the growing and unavoidable fiscal demands being placed on the Fed.”