11

11

The crypto derivatives market is sending an unusual signal: directional longs and directional shorts are nearly equal, a condition analysts say is historically unsustainable and could foreshadow a major shift ahead.

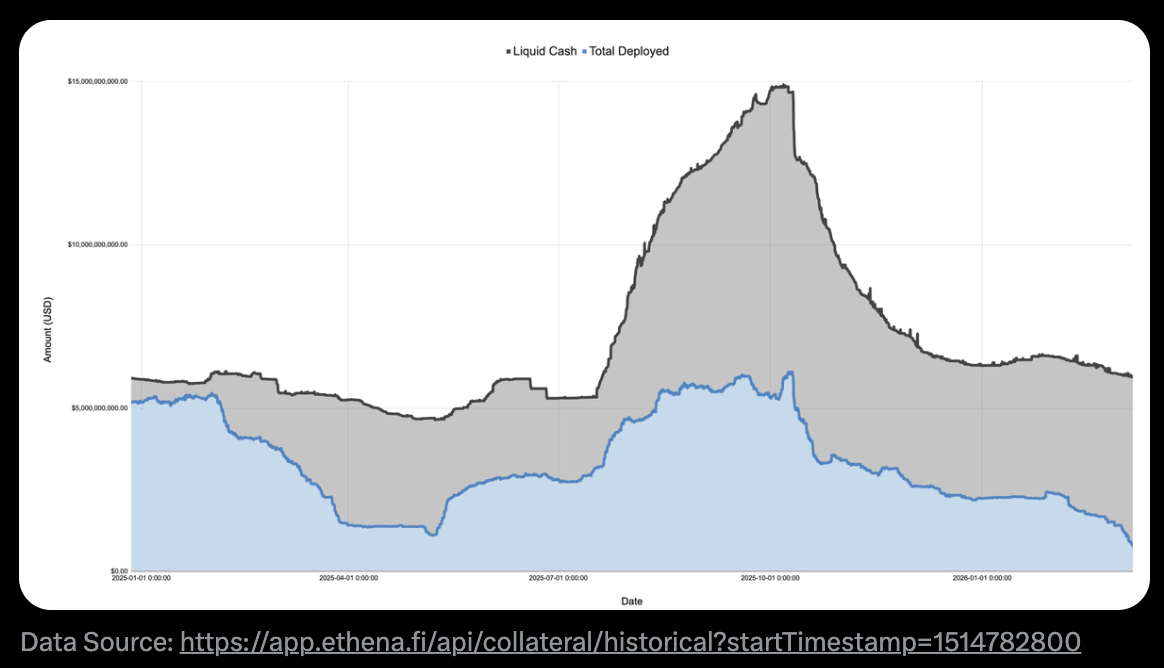

According to an analysis published by WuBlockchain yesterday, data from synthetic dollar protocol Ethena's transparency dashboard reveals that deployed capital, a proxy for excess long demand in futures markets, has fallen to just $791 million, down more than 85% from its all-time high.

Since Bitcoin's crash to $60,000 on February 8, Ethena's basis position has shrunk by over 60%, dropping from more than $2 billion to under $800 million, even as the broader market has remained relatively flat.

Ethena operates by taking the short side of perpetual futures contracts against leveraged long traders, effectively running the classic crypto carry trade at scale. When demand for leveraged longs outstrips natural short interest, Ethena steps in to absorb the difference. Its shrinking book, therefore, implies that directional shorts and hedgers are increasingly filling the role that basis traders once dominated.

The author of the analysis, SoskaKyle, attributes the shift largely to a growing wave of hedging activity from crypto VCs and smaller projects seeking to protect their treasuries and lock in gains. With hundreds of small-cap tokens, each backed by dozens of investors and teams needing to manage their runways, the result has been a crowded trade: actively managed structured products that short baskets of correlated assets.

While this near-parity between longs and shorts could theoretically persist, history across asset classes suggests it rarely does for long, leaving the market a potential inflection point.

This article was written with the assistance of AI workflows. All our stories are curated, edited and fact-checked by a human.