23

23

The December Producer Price Index didn't just beat expectations, but it also revealed a persistent problem that forces markets to rethink the entire 2026 rate path.

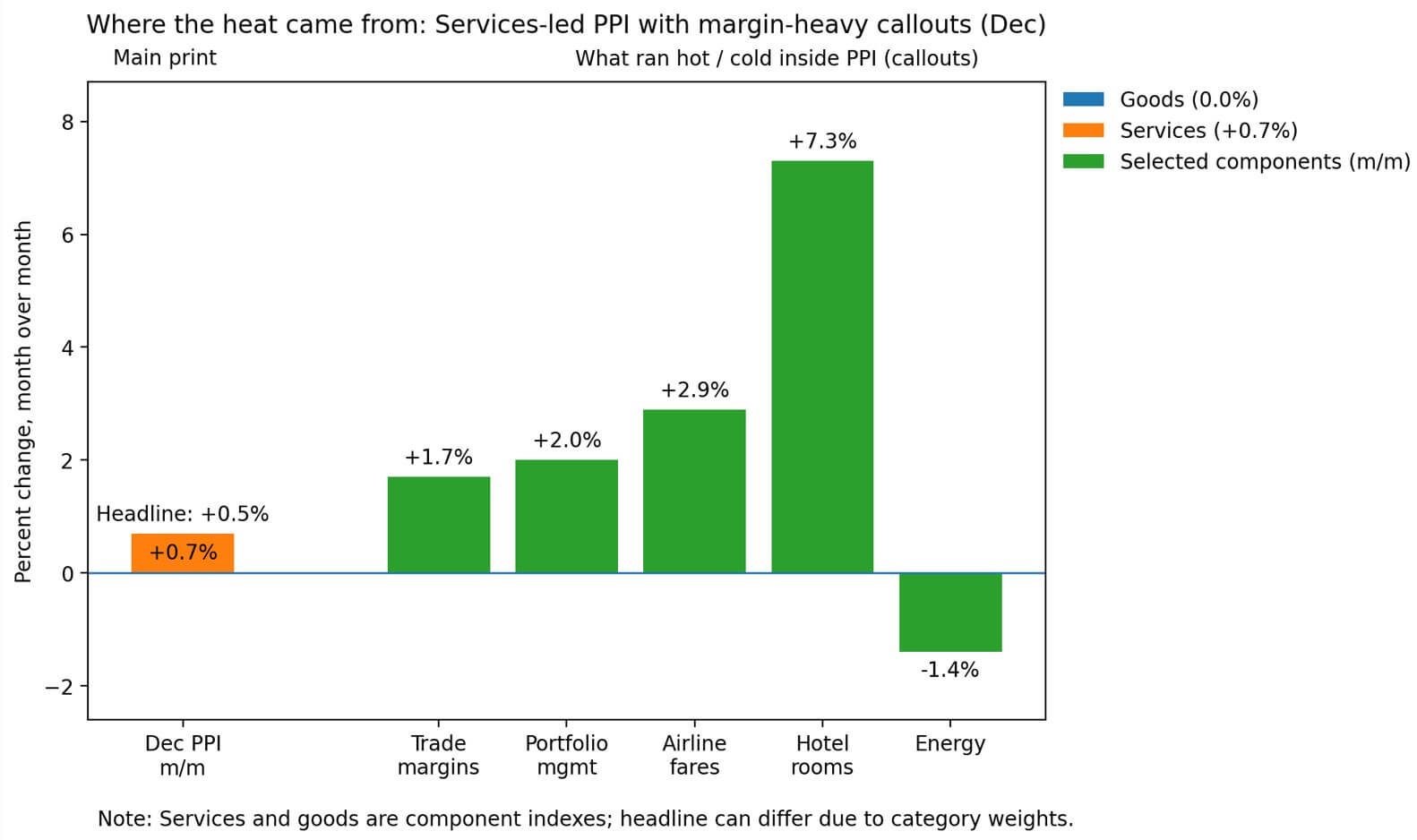

Final demand PPI rose 0.5% month-over-month, the sharpest jump since July, driven almost entirely by a 0.7% surge in services while goods prices sat flat. The headline came in at 3.0% year over year, beating expectations of 2.7%, but core PPI rose to 3.3% from 2.9%, the highest level since July 2025.

Markets sold the news immediately. Bitcoin dipped below the $82,400 zone as it was trying to recover from an intraday low of $81,100. Meanwhile, Fed funds futures repriced to just 52 basis points of cuts for all of 2026, with the first quarter-point move now pegged for June.

The dollar index is up 0.82% over the past 24 hours, and real yields on 10-year TIPS are near 1.90%.

This raises the question of whether this confirms that disinflation has stalled in the exact place the Fed can't ignore: services, where pricing power is sticky, and margins are expanding rather than compressing.

What actually ran hot and why it matters

December's report revealed sustained pricing power rather than transitory shocks.

Trade services margins, which are the spread between what wholesalers and retailers pay versus what they charge, jumped 1.7%. Portfolio management fees climbed 2.0%, airline fares rose 2.9%, and hotel rooms spiked 7.3%.

These aren't categories buffeted by volatile commodity prices, but rather areas where firms successfully pass costs through to end users.

Energy fell 1.4%, which normally would drag the headline lower. Instead, the service's strength overpowered it. Even stripping out trade, transport, and warehousing, services still rose 0.3%.

The Bureau's narrowest core measure rose 0.4% for the eighth consecutive month, bringing the year-over-year rate to 3.5%.

Eight straight monthly increases in the stickiest subset of PPI argue against dismissing this as noise. Trade margins can reverse quickly if demand weakens, but the broader services prints suggest firms retain pricing power across multiple categories.

That's the inflation the Fed targets when it talks about the “last mile” problem.

The PPI-to-PCE bridge and the Feb. 20 gate

Producer prices don't directly set monetary policy, as the Federal Reserve monitors Personal Consumption Expenditures inflation, which is released on Feb. 20. However, PPI components are mechanically incorporated into PCE calculations.

Portfolio management, airfares, and lodging all show up as inputs to core PCE, meaning December's hot PPI creates an upward tilt for the print markets that will be scrutinized in three weeks.

Economists currently estimate that December core PCE is between 0.3% and 0.4% month over month, implying approximately 3.0% year over year.

The Cleveland Fed's nowcast tracks January 2026 core PCE at roughly 2.76% year-over-year. The value is still above the Federal Reserve's 2% target, but not accelerating into the mid-3% range that would prompt an immediate hawkish pivot.

Government shutdown disrupted data collection and necessitated the BEA's approximation of missing CPI inputs for October's PCE report. Revision risk is higher than usual, which means the first print on Feb. 20 might not be the final word.

Markets hate ambiguity, and ambiguity around the Fed's preferred inflation gauge keeps real yields elevated and risk assets volatile.

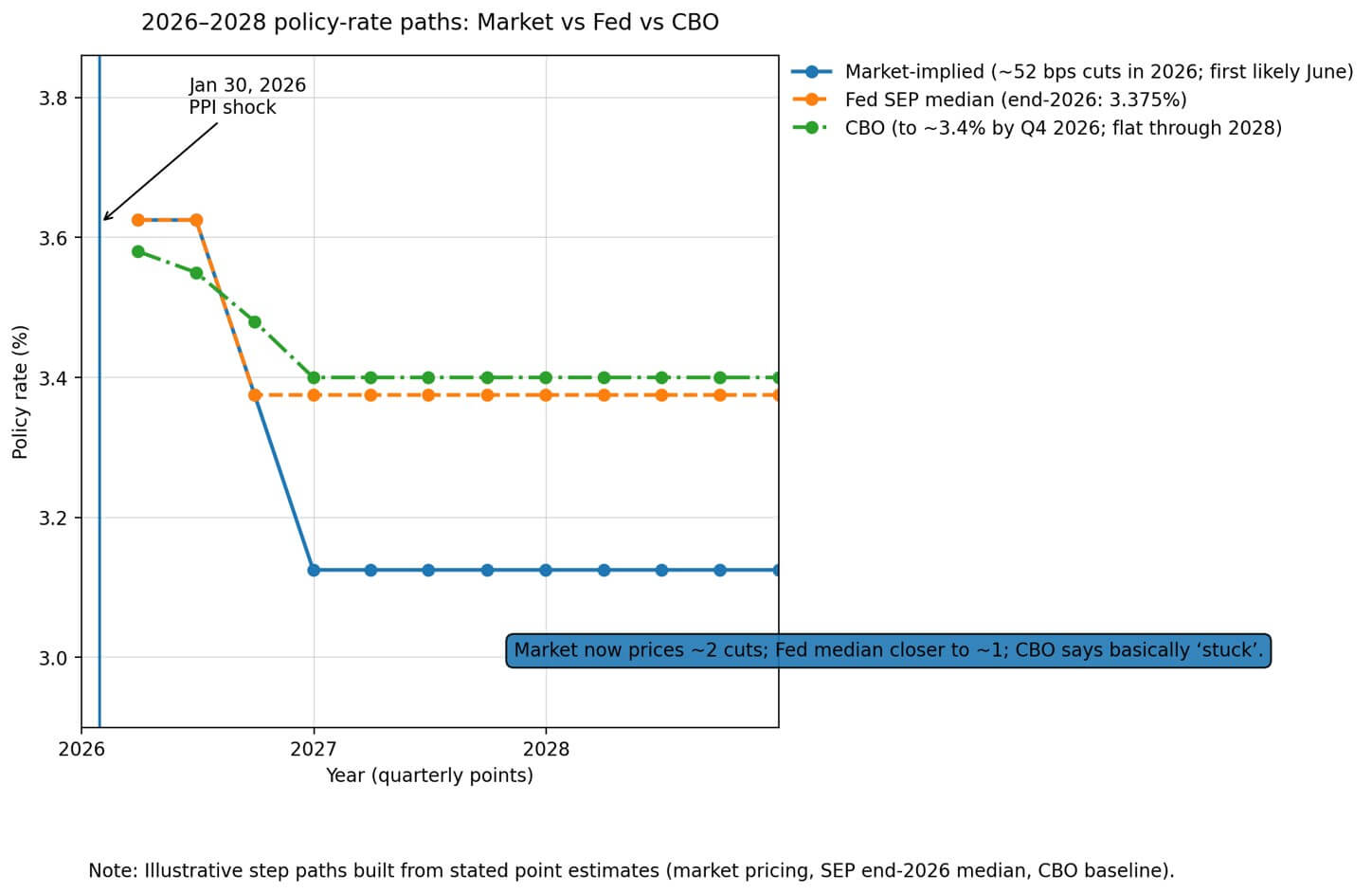

What the market now believes

As of Jan. 30, Fed funds futures price approximately 52 basis points of cuts across 2026, with two quarter-point moves, the first likely in June. The market assigns less than 30% probability to cuts in March or April and around 65% to a June move.

Compare that to the Fed's December Summary of Economic Projections: the median participant saw the policy rate ending 2026 at 3.375%, roughly one cut from today's 3.50%-3.75% range.

The Congressional Budget Office (CBO) projected that the policy rate would drift to about 3.4% by the fourth quarter of 2026 and remain flat through 2028, with inflation remaining above 2% for years due to tariffs and tax cuts.

The market is pricing slightly more easing than the Fed's median dot, but far less than the “normalization” path some had hoped for.

The CBO's projection implies that inflation won't cooperate even with modest easing. Rates stay higher for longer, not because the Fed is hawkish, but because the economy won't deliver the disinflation needed to justify deeper cuts.

Three scenarios for rates and Bitcoin

The base case for rates and Bitcoin consists of two cuts, starting in June.

Feb. 20's PCE comes in at around 0.3%-0.4% month-over-month, confirming sticky but not accelerating inflation. The Fed cuts twice, by roughly 50 basis points, keeping policy restrictive enough to contain inflation without choking growth.

For Bitcoin, this translates to choppy conditions. Higher real yields and a firm dollar create opportunity-cost drag, but a glidepath of two cuts isn't outright tightening.

The hawk case is “higher for longer.” Feb. 20's core PCE prints 0.4% month-over-month, and the following months don't cool. Services inflation stays broad, and the Fed delivers just one cut or none.

Markets reprice toward zero or one moves, real yields rise, and the dollar strengthens. Bitcoin faces a clear headwind. Dollar strength correlates negatively with Bitcoin returns, and the absence of expected easing pressures crypto prices by raising the hurdle rate for speculative assets.

For the dove case, disinflation resumes, and growth softens. December and January core PCE come in near the 0.2% month-over-month trend from mid-2025, labor markets show cracks, and the Fed can “catch up” on cuts.

Three to five cuts, 75 to 125 basis points, become plausible. Real yields fall, the dollar weakens, and risk appetite rebounds.

Bitcoin would benefit from easier financial conditions, though the initial trigger of growth weakness could create a risk-off shock before the dovish repricing takes hold.

| Scenario | Base | Hawk | Dove |

|---|---|---|---|

| Feb 20 core PCE signal (gate) | 0.3%–0.4% m/m (sticky, not accelerating) | ≥0.4% m/m and follow-through risk (services stays broad) | ~0.2% m/m trend resumption + softer activity |

| 2026 cuts (policy path) | ~50 bps (≈2 cuts), starting June | 0–25 bps (0–1 cut), “higher for longer” | 75–125 bps (≈3–5 cuts), earlier/steeper easing |

| Real yields (10y TIPS) direction | Flat-high (stays elevated) | Higher (tightening via expectations) | Lower (policy + disinflation pull real rates down) |

| Dollar (DXY) direction | Firm (rate differential stays supportive) | Stronger (higher real-rate premium) | Softer (differentials compress, liquidity improves) |

| $BTC bias | Choppy / range-bound (opportunity-cost drag offset by “not tightening”) | Headwind (higher hurdle rate + stronger USD) | Tailwind (easier conditions), but watch initial risk-off if growth cracks |

| What to watch next (2-week checklist) | Confirm: 10y real yields + DXY move together (or not). Validate: $BTC stops making lower lows when yields stabilize. Risk: PCE revision risk (shutdown distortions). | Confirm: real yields make new highs and DXY breaks higher. Validate: $BTC fails to reclaim key levels on bounces. Risk: “higher for longer” rhetoric hardens before/after Feb 20. | Confirm: real yields roll over and DXY softens. Validate: $BTC strength persists beyond one-day relief. Risk: if dovishness = recession shock, $BTC can wobble before repricing helps. |

What changes for crypto positioning right now

The tactical question isn't whether to make a directional bet, but whether the post-PPI repricing creates a durable shift in the macro dials that matter for Bitcoin.

Two variables provide the cleanest read: real yields and the dollar.

Real yields on 10-year TIPS sit around 1.90%, well above the sub-1% levels that prevailed during Bitcoin's 2020-2021 rally. As long as real yields stay elevated, the opportunity cost of holding Bitcoin remains high.

The dollar index at 96.92 reflects global liquidity conditions. If “higher for longer” plays out, the US dollar should strengthen as US real rates remain elevated.

If the dovish scenario materializes, the dollar should weaken as rate differentials compress.

The cleanest signal would be confirmation across both. Real yields and the dollar moving in tandem, followed by sustained Bitcoin weakness or strength.

Jan. 30's price action of dollar up, yields up, and Bitcoin down to a two-month low fits the hawkish repricing narrative, but one day doesn't make a trend.

The next two weeks leading up to the Feb. 20 PCE release will show whether markets commit to that view or revert to range-bound uncertainty.

December's PPI raises the stakes for the Feb. 20 PCE release.

If services inflation proves as sticky as this report suggests, the Fed's ability to ease in 2026 narrows considerably. Not because officials want to stay restrictive, but because the data won't cooperate.

For Bitcoin, the question isn't whether it can rally despite higher real yields, since it has before. The question is whether the base case for 2026 now assumes tighter-for-longer conditions as the default.

The market is pricing 52 basis points of cuts, but that's a median expectation with wide tails. The Fed holds the trigger, but inflation data will decide whether it gets pulled twice, once, or not at all.